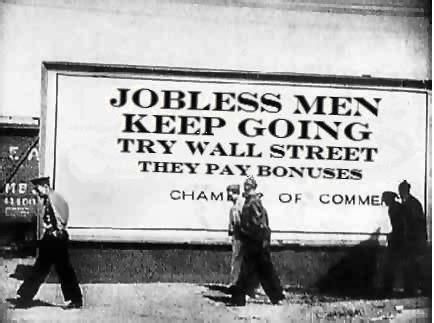

MEDIA ROOTS — “Both parties have conspired to bring us disaster,” says Professor William K. Black, a leading white collar criminologist, who also teaches economics and law at the University of Missouri-Kansas City. “This has strangled the recovery and may even put the economy back into recession.” Professor Black gives a crucial recap of Obama’s (and both Democrats’ and Republicans’) recent history of assaults against the working-class, also known as austerity.

This “act of austerity is insane, self-destructive, [and] might well cause another recession,” says Prof. Black. “Neither party is getting behind a clean bill. It would be, literally, one sentence: The sequestration provisions are repealed.”

With the fast-paced 24-hour soundbite news cycle dominating attention spans, it’s beneficial to take a step back and scope the bigger picture. Professor Black masterfully articulates the truth behind the two-party budget cuts at home coupled with war spending abroad.

Messina

***

Prof. Bill Black: Both parties have conspired to bring us a disaster; Obama’s sequestration plan gives cuts without blame

***

REAL NEWS NETWORK — “Welcome back to the Real News Network. I’m Paul Jay in Baltimore. And welcome to this week’s edition of The Bill Black Financial and Fraud Report. [Professor] Black now joins us from Kansas City, Missouri. Bill’s an Associate Professor of Economics & Law at the University of Missouri-Kansas City. He’s a white-collar criminologist, a former financial regulator. He is the author of the book, The Best Way to Rob a Bank Is to Own One. Thanks for joining us, Bill.”

Professor Bill Black: “Thank you.”

Paul Jay (c. 0:33): “So, the sequestration cuts and drama, what do you make of it?”

Professor Bill Black: “So, both parties have conspired to bring us disaster. In this case, sequester is the fourth shoe to drop in austerity. And, collectively, this has strangled the recovery and may even put the U.S. economy back into recession.

“So, the first major act was in mid-2011 when they reached this budget deal, that created the sequestration. And the budget deal, in itself, caused over a billion dollars in spending cuts at the worst possible time.”

Paul Jay (c. 1:15): “So, just to remind everybody, the sequestration formula deal was a proposal by President Obama.”

Professor Black: “Well indeed, it was created by President Obama, now, under, of course, Republican pressure, where they’re threatening to not raise the debt ceiling. But it was an Obama idea. And the principal framer of it was Jacob Lew, the President’s selection to be Geithner’s replacement as disastrous Treasury Secretary.

“And then the President blocked a Republican effort to get rid of sequestration. And then the President went so far as to threaten a veto any bill, that got rid of sequestration when the Republicans tried to get rid of it again.

“Now, you shouldn’t think too well of the Republicans in all of this. What they were worried about, pretty much solely, was defence spending. And making sure there’d never be a drop in defence spending.

“In any event, what you see is neither party, even at this time of crisis, where all the supposedly serious people finally agree that this act of austerity is insane, self-destructive, might well cause a recession. Neither party is getting behind a clean bill. It would be, literally, one sentence: The sequestration provisions are repealed. Right? And we could be free of, at least, that aspect of the insanity. We’d still have the debt ceiling insanity. But the sequestration, we would no longer be shooting ourselves, not in the foot, but substantially farther up our anatomy.

“So, as I said, the sequestration is large, but it’s not the sequestration all by itself. It’s the fact that it is this fourth act austerity. I began to mention the mid-2011 pact knocked off a billion dollars in spending at the worst possible time.

“Then we raised taxes on the wealthy, which you may well support, but it is an act, that pushes you towards austerity.

“And then the far larger and vastly more destructive resuming the entire payroll tax on Social Security, which economists think—all by itself—knocked a half percentage point off of growth. And growth is really small, so that’s a massively important thing, that is gonna cost hundreds of thousands of people their jobs.

“And, now, the fourth shoe to drop of austerity, of course, is going to be the sequestration.

“And, meanwhile, this is happening while we see Europe forced back into a completely gratuitous recession. The entire Eurozone, on average, is back in recession. And the European Commissions have just come out with dreadful projections, saying things are going to get worse.

“Spain just announced today that a single bank that they were bailing out—which is really seven failed thrift-type entities—is going to cost them roughly $25 Billiondollars just this year. And Spain’s a large economy, but nowhere close to the United States.

“So, this is bigger, by far, than the most expensive US banking failure in history, all occurring in Spain, all being driven by the bubbleand fraud and then this self-inflicted wound of austerity.

“And we can’t even get the President, who, you know, on day one will say, the sequestration disaster [is] insane.

“And on day two refuses to put forward a clean bill to stop it.

“And, on day three, says, hey, that Jake Lew, the guy, that created this disastrous scenario, that is going to, potentially, hurl us back into a recession. He should be our Treasury Secretary and create our financial policies.”

Paul Jay: “So, when you read the business press, some of the stories are about how blasé Wall Street is and corporate America is. And they’re not very concerned with $85 Billion dollars of cuts. And the stock market’s doing fine. It does not seem to be affected by it. Why is that, if the threat of recession is looming?”

Professor Black (c. 5:53): “Well, recession isn’t necessarily bad for the stock market. We’ve had a record recovery in stock market prices with extremely weak recovery from the Great Recession because it’s been strangled.

“So, they love the current system, in which wages have not simply plateaud, household wealth for the middle class is down to where it was 18 years ago. There’s over a 15% of loss of wealth of the middle class and working-class and a massive increase in corporate profitability where we get all these productivity gains, which is what allows you to pay workers higher wages without any inflationary risk. And virtually all of those productivity gains during the Great Recession have gone to the richest—not 1%—but the richest one-thousandth of 1%.”

Paul Jay (c. 6:54): “Thanks very much for joining us, Bill. And thank you for joining us on the Real News Network.”

***

Transcript by Felipe Messina for Media Roots, New Economic Perspectives, and Real News Network.

MEDIA ROOTS — The top 1% hold 40% of the nation’s wealth. But the bottom 80% hold only 7% of the nation’s wealth. This infographics video provides an arresting presentation of widening wealth inequality in the USA. It also compares and contrasts our perceptions with actual reality.

A notable segment is a graph showing perfect equality, which is summarily disregarded by our society because it’s labelled socialism. The logic goes that people need protive motive, which means we choose to have socially-stratified classes, where we always have a lower class, an underclass. However, we only hear about the mythologised middle class in our national discourse. This means we idealise having an elite, ruling-class as well, to which we’re supposed to aspire entry. However, when over-allocated crony capitalists prey on the working-class (which includes the celebrated middle class), we wonder what went wrong.

MEDIA ROOTS — Obama’s attacks on the social safety net continue, fueled by the claim the USA is running out of dollars. During the recent Steinhardt Lecture at Lewis & Clark College in Oregon, UMKC Professor L. Randall Wray debunked various economic myths marketed in today’s headlines, which are enforced in universities and echoed by the Obama Administration. These same myths provide pretexts for “fiscal austerity” and “sequestrations,” against the backdrop of giveaways for the ruling-class.

Yet, we come to find, government spending during a recession doesn’t hurt the economy and the US doesn’t ‘borrow dollars from China.’ In the midst of the currently raging debate on “sequestration,” Dr. Wray presents very important economic perspectives the nation needs to understand in order to read between the lines of Washington, D.C. doublespeak.

Messina

***

NEW ECONOMIC PERSPECTIVES — L. Randall Wray recently presented at the Steinhardt Lecture at Lewis & Clark College in Oregon. The title of his presentation was: “Fiscal Cliffs, Debt Limits, and Unsustainable Deficits: Can the US Really Run Out of Dollars?”

Dr. Wray’s Lecture’s accompanying slideshow

***

2013 Steinhardt Lecture, Lewis & Clark College, Oregon:

Eric Tymoigne: “Alright. Good evening, everyone. My name is Eric Tymoigne. I am an Assistant Professor at the Department of Economics. And, on behalf of the Department, I am pleased to welcome you to the Steinhardt Lecture. It is the 42nd Steinhardt Lecture; and it is named in honour of Herman Steinhardt, the first Chair of the Economics Department at Lewis and Clark College.

“Herman Steinhardt was a businessman working in textiles in Austria during the 1930s. He and his wife, who [were] Jewish, were forced to leave the country because of the growing Nazi threat. Unable to find a job in textiles, in the United States, he decided to pursue an academic career. After receiving a degree in economics, he was hired as a professor and a chair at the college. He retired in 1964.

“To honour his many years of service, friends of the economics department established a lecture series in his name in the 1970s. The Steinhardt Lecture is given every February by a distinguished scholar, chosen by the economics department and faculty. And the purpose of the Lecture is to engage in public policy issues.

“The 2013 Lecturer is Dr. L. Randall Wray. He is a Professor of Economics at the University of Missouri-Kansas City. Dr. Wray is also a Senior Scholar at the Levy Economics Institute and the Research Director of the Center for Full Employment and Price Stability [C-FEPS].

“He has published numerous articles and books on a variety of topics, including such [things] as Social Security, banking, the history of money, full employment policies, and financial crises. His two most recent books are Understanding Modern Money: The Key to Full Employment and Price Stability and Modern Monetary Theory: A Primer on Macroeconomics for Sovereign Monetary Systems.

“Tonight’s Lecture will address issues surrounding the public debt and budget deficits, which, are currently subject to heated debates in Washington. Please join me in welcoming Dr. Wray. [Applause]”

Dr. L. Randall Wray: “Well, thank you for coming out. And thank you for inviting me here to give this talk. I’m sure that you’re all reading in the newspapers and watching on TV the debates about the US government budget. So, I’m going to try to answer the question: Can the the US really run out of money? Is this much ado about nothing? Or maybe something to do about a little?

(c. 3:09) “So, President Obama, for a long time, actually, even before the current debate, argued, that ‘our government is running out of money.’ He would like to do more to help the economy, to help the unemployed, but Uncle Sam has run out of money. Economists argue that we’re on an unsustainable debt path. And most Americans seem to have come to some kind of an agreement with these two positions. I just saw, in the hotel this morning, a USA Today poll says 70% of Americans say progress on the deficit is needed this year. And it was by far and away the topic, that had the greatest percent of Americans agreeing this was an issue, a critical issue, that needs to be resolved very quickly. Nothing else was even 50%.

“There’s this fear we hear all the time that we’ve been borrowing from the Chinese and someday they might stop lending to us and we would be in trouble. We have a lot of people arguing that the big budget deficits today, and in the future, are threatening us with hyperinflation. So, we might suffer the fate of Zimbabwe or the Weimar Republic.

“Many people argue that that debt is a burden on our grandkids.

“And, finally, people point their fingers to Europe and say, that could happen to us. We might have a sovereign debt crisis, like the Irish, the Greeks, the Italians, the Spanish. There is rising default risk on these nations’ debt.

“And the bond vigilantes are attacking them, boosting interest rates, increasing interest payments on the debt, and imposing conditions on these countries, forcing Greece to sell off its national heritage in order to try to cover interest payments, that the vigilantes are demanding.

“Is any of this true?

“Mark Twain said, ‘It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just aint so.’

“So, I’m going to be arguing, it just ain’t so. What we think we know is not true.

“First, I’m going to show you some pieces of data. And then we’ll get into the more theoretical arguments. I’m gonna try to not make it any more wonky than we have to make it.

(c. 5:58) “We’ve had a debt limit in the United States for about a hundred years, that was imposed by Congress on itself. If you think about it, it’s sort of a strange thing. Every year Congress proposes a budget and they get the President to sign off on it. And that tells them what programmes are gonna be funded, up to what limit. And then we have some spending, such as on Social Security, that depends on people meeting the requirements of the programme and then they get their checks.

“But, in its wisdom, Congress decided that wasn’t enough, the budgeting process isn’t enough to constrain government. So, they also imposed a debt limit, so that, as the federal government debt rises towards that limit, then Congress has to get together and agree to raise the limit, so that Congress could spend the money—sorry—the Administration can spend the money, that Congress already told it to spend. It’s a strange thing. Other countries don’t do this.

“Normally, it didn’t matter because the Democrats and Republicans would get together and raise the debt limit and life would go on. And the Administration would spend the money already budgeted.

“But the Republicans, together with some Democrats, decided to make it an issue. And, so, we had, a couple years ago a, big debate about raising the debt limit. And a compromise was created to create a fiscal cliff. And the thinking—you’ve heard all of this so much I don’t need to go into it in detail—the thinking was we’ll make it so terrible that come January 1st, 2013, they’ll get their act together and agree to impose budget cuts as a compromise to increasing the debt limit. Well, January 1st came and went and they didn’t do it. So, instead what they [said] was, lets give a two-month extension to March. And we’re going to immediately go ahead and raise the payroll tax, so that up to $2,000 per year will be taken out of paychecks.

“Essentially, what they were doing was just taking back the payroll tax holiday, that they had given to try to stimulate the economy.

“So, anyway, now we’re waiting to see what happens in a few days. If they don’t come to an agreement, we’re gonna have $1.2 Trillion dollars in budget cuts imposed. Half of that is on domestic spending and the other half is on military spending. If you listen to NPR, this morning they were talking about laying off air traffic controllers. And I fly a lot. And this is pretty scary. But just across the board cuts. And that was on purpose. It was to make this extremely painful, so that we would never get to the point that we’re at—and already missed one deadline.

“Anyway, it’s gonna reduce GDP by about 1% directly. And, in spite, of what we were told by some economists, even the IMF has come out and said, you know, wow, there really is a government spending multiplier. If you cut government spending, GDP goes down by a lot more than the cut of government spending. There is a spending multiplier. And, so, that’s going to hit us, too, so, that the effect on GDP is gonna be greater than 1%.

(c. 9:30) “Okay, so, the question is:

“Is there really something we should be worried about?

“Is there any evidence that our government has been taken over by hyperinflationaries?

“Are we on a path to Weimar or Zimbabweland?

“Is debt at a historic high?

“Is government spending out of control?

“Have we really hocked ourselves to China?

“Does the debt burden really burden our grandchildren?

“Will entitlements bankrupt our grandkids?

(c. 10:06) “So, let’s look at data first, as I said. [See accompanying Slide Show]

“Here’s a picture of US federal government debt from 1950 to approximately the present. The red line shows the total amount of debt. But the government owes itself a lot of that debt. Okay? And this is Social Security and, increasingly, the Fed. There are pretty good reasons not to include debt, that the government owes to itself in the calculation. But, if you want to, you’ve got both of them here. And you can take a look.

“You can see that the gap between the two is growing because the goverment owes itself even more and more and more, like you owing yourself. You can decide whether that matters much or not. In any case, no, we’re not at a historic high. Okay? We were much higher in 1950. And you can see how rapidly the debt ratio went down after 1950. You might think that it’s because we paid off World War II debt. And the answer is, no we did not.

“It came down because GDP grew. We reduced the debt ratio by growing the economy. The debt, that we ran up in World War II is still out there, almost all of it. In fact, if you go back to the founding of the country, there’s only been one time, in wich we actually did pay down the debt. That was in 1837. We never did it again. All the debt, that we’ve issued since then, still pretty much exists. Okay?

“But we’ve lowered the debt ratio by increasing economic growth. You could see that the debt ratio really spiked up when the crisis hit. And I’ll talk more about that in a second.

“Many people think that we had such big fiscal stimulus packages and that when Obama came in—of course, he’s a Democrat, which means he must be a big government spender—and, so, the rise of the deficit up to 10% of GDP and the resulting rise of government debt is because of all the discretionary spending, that Obama has put into place. The reality is quite different from that.

“What actually happened is that tax revenue fell off a cliff. The tax revenue fell off a cliff when we went into the very deep recession, the worst since the 1930s. Tax revenue, if you go back, if you can read the numbers back to 2005, tax revenue was growing above 20% per year, phenomenal growth of tax revenue. And, actually, at the time, I wrote that this is going to kill the economy. And in two years it did.

“So, the tax revenue is growing very fast. And then we hit the cliff. We went into a deep recession. The tax revenue disappeared. That is why the budget deficit blew up. There is a bit of a fiscal stimulus. But it’s very, very small compared to the decline in tax revenue. And the automatic stabilisers, transfer payments, like unemployment compensation kicked in because of the recession. So, that’s the top blue line, that goes up, the transfers payments, and unemployment compensation, and food stamps when people lost their jobs and their incomes.

“So, actually, the deficit increase and much of the growth of debt is because the economy has been rotten. If the economy recovered we would expect that tax revenue would go up. And, actually, you notice that tax revenue growth did go up in the last couple of years, as the economy recovered a little bit and as the unemployment rate declined a little bit.

(c. 14:03) “The story about Obama, big deficit spender, fiscal stimulus leading to the big deficit, also doesn’t fit the facts of this one. This is a very unusual recession and attempt at a recovery, in that it’s only in the very beginning when we had a fiscal stimulus, the lighter blue line. Since then, the government, actually, has been a drag on the economy, very unusual, we haven’t had recoveries, since the Ronald Reagan years, in which the government, actually, was a drag on the economy, trying to come out of a recession.

“Here’s another one [slide], the growth in real per capita government spending. Precisely, the opposite of what is commonly said, Obama is not the big government spender. He, actually, has reduced government spending in real terms per capita, while no other previous president going back to Nixon and Ford had done that.

“So, the deficit was not due to government spending. The government, actually, continues to take demand out of the economy, as it now is pulling jobs out of the economy. So, job growth, government job growth, is actually negative.

“Okay, let’s look at the story about we’re at hock to the Chinese. Some of the older people here can remember back in the ‘80s, ’90s, and through the early 2000s, when the same stories were told about the Japanese when the Japanese were accumulating US Treasuries. And there was a great fear that the Japanese would start being the owners of the United States and that we would be controlled by our creditors, who are the Japanese.

“Now, the same story is told about the Chinese. And you can see, earlier on, the Japanese were the big holders and they have declined, as China has become the big holder.

“First, the stories about the Japanese controlling us because they were our creditors never came true. It never happened.

“Second, why is it that, first, the Japanese and then the Chinese become big holders of US government debt? You know? There must be some similarity, some explanation for why that happened. And this picture [PowerPoint slide #12/39] is a little complicated. You might want to look at it in more detail later when it’s posted up on the website.

“I only want to draw your attention to the two top curves over here [pointing to screen with laser pointer]. So, this is showing US Treasury debt held by the rest of the world. Okay? The blue. The other one, you could see, [which] tracks it fairly well, is our current account balance, like our trade deficit?

“So, our trade deficit is very highly correlated with foreigners holding US Treasuries. When we import more than we export, the foreigners, the big, exporting foreigners, who export stuff to us, end up holding a lot of US Treasuries. Okay? Why is that?It’s because they want to sell stuff to us in order to get very safe, dollar-denominated, financial assets. Okay?

“In the first instance, for reasons I’ll explain in a bit, they initially get reserves, which are deposits at the Fed. And those reserves at the Fed don’t earn any interest. The next-best thing they can get are US Treasury bonds. And those do earn interest.

“So, what they do is they trade the reserves at the Fed for US Treasury bonds. And it’s not a surprise at all that the Chinese will end up with US Treasuries when they are exporting Chinese goods to the United States. Okay?

“So, we can explain it perfectly. As long as China wants to run a trade surplus—export to the US more than they import—they will be accumulating US Treasuries. When they change their minds and decide they would rather be consuming the goods themselves than sell it to us, they will stop exporting to the US and they will stop accumulating US Treasuries.

“There’s no imbalance here. It is a balance. They’re doing it because they want to do it, whether it’s in their interest or not is not for us to decide. But, as long as they’re wiling to send us their output, they will accumulate Treasuries.

(c. 19:24) “Now, earlier, I was saying that you do expect the budget deficit to go up when times are bad. And that as we recover tax revenues will go up. That’s already happening. The budget deficit will decline. It’s already happening. The budget deficit declined from about 10% of GDP to about 6.7% of GDP. So, it’s already happening. If we continue to recover the budget deficit will go down. It always has in recoveries. It always will.

“But people say, that’s not our real problem. The problem is not the deficit today. The problem is the long-run deficit, the chronic deficit, that we are stuck with. And that is mostly because of entitlements. It’s because of Social Security and Medicare.

“I’d love to spend the whole 90 minutes talking about those two programmes because there’s so much misconception out there. And it goes beyond misconception—purposely misleadingpeople about those programmes. But I don’t have time to do that. I gotta stick to the fiscal cliff.

“But, anyway, the argument is the budget deficits and rising debt is a problem for the long run. They will continue to go up as baby boomers retire and even beyond that. Some economists carry this all the way to—they do what is called am infinite horizon forecast. It’s not enough to look 70 years into the future, they say. We have to look to an infinite future. So, we project Social Security revenues and spending and Medicare revenues and spending, not for 20 years, not for 70 years, not for a thousand years, forever. They project them forever.

“And then they discount that back to the present. And then they tell you, the programme is $70 Trillilon dollars short.

“Anyway, whether we should worry about that or not, you know, is a completely different matter. What I’m gonna—the forecasting, your ability to do that, and whether the United States will survive forever, I don’t know.

“But, as a way of introduction to the topic about whether its true that budget deficits are unsustainable, whether the federal government could continue to run deficits and accumulate debt outstanding, let’s go back to the fairly recent past—President Clinton—because we’re almost in the opposite situation today, as we were in the late ‘90s. In 1996, the US federal government started to run a surplus and continued for two and a half years, a significant surplus. And I know a few of you will know the answer to this. When was the last time the US federal government ran a significant surplus for more than one quarter? [Inaudible audience member]

“There we go! Right before the Great Depression. Right before the Great Depression. Well, we ran this one right before the Great Crash or sometimes it’s called the Great Recession.

“Anyway, so we ran a budget surplus and Clinton thought this was a great thing and some of you will remember him going on TV projecting we’re gonna run a budget surplus for the next 15 years. And it’s gonna be so large, we’re gonna retire all the government debt, so that we will be completely free of federal government debt for the first time since? 1837, which was followed by our first Great Depression, which most people forget about because it was a long time ago.

“Anyway, all the government debt will be retired. But, you know, it wasn’t all quite rosy because private debt exploded while the government was running a budget surplus. And then, of course, we crashed into the recession after the NASDAQ collapsed and the budget deficit was restored. And everyone had sort of forgotten about this. You know; could you imagine a worse projection? Because right now, today, we should have no government debt, or we should be very close ‘cos we’re about 15 years out. We should be free of government debt. How good was that forecast? Pretty far off. Okay? Pretty far off. And, in fact, we started running a budget deficit soon after he made the statement. He made the statement in 1999. And, by 2000, we were running a budget deficit.

“Okay, why? Why this link between a budget surplus and a private sector deficit? It’s because balances balance.

(c. 24:27) “In 1999, I saw, in The Wall Street Journal, a fantastic article, or fantastic pair of articles. On the left-hand side [of slideshare slide #15/39], I know this is going to be hard for you to read. But it says:

“Budget surpluses may wipe out the government debt, says President Clinton. Okay? Left-hand side.

“And then the article goes on to say:

“Isn’t it fantastic that the government finally is adding to the national savings by spending less than its income? For the first time. (They didn’t say since 1929.)

“On the right-hand side, it says:

“The savings rate declines, again.

“They say, isn’t it terrible that the private sector households are spending more than their income? Isn’t it terrible? And then they give you a nice little picture right in the middle, between the two, that shows you government going from negative saving to positive saving and the private sector going from positive saving down to negative saving. And neither of the articles mentions the obvious question. Could these two things be linked? Well, yes, they are, by identity.

“If the government sector runs a surplus, the non-government sector has to run a deficit. It’s by identity. And here’s the identity. Again, we don’t want to get too wonky, but when we think about the domestic sector, its overall balance has to equal the foreign sector’s overall balance. I know a lot of people don’t like algebra, but pictures are nice. Okay. Here’s the picture [slideshare slide #17/39].

“And what’s the first thing you notice about the picture? It’s a mirror image. Hey, balances balance. Isn’t it nice when the real world cooperates with the theory, or the identity? It has to be true. For everything above zero, there is something below zero, exactly, dollar for dollar. Okay?

(c. 26:40) “The second thing you notice is, boy, there’s a lot of red below the line. That is the US federal government deficit. Whenever the red is below the line, the government is running a deficit. Whenever the red is above the line, the government is running a surplus. And what do you know? The government, well, almost always runs a deficit, almost always—and that’s always been true for the US federal government. There is a period there, that stands out, where the red is above the line, above zero, which means there’s a budget surplus; that’s Clinton. That’s when he’s announcing, we’re gonna do this for the next 15 years. Imagine how much, how big those surpluses would have to have been to offset all of the reds on the other side. Okay? But that’s what he thought he was gonna do.

“Okay, so, a very brief period. And it’s the only one you could see. Okay?

“The blue is the private sector. That’s households and firms, taken together. If the US was a closed economy, there was no foreign sector, the reds would have to, exactly, be balanced by the blues. Anytime the red is below the line, the blue must be above the line, if there’s no foreign sector. So, set aside the foreign sector—that’s the green—just for a minute.

“You could see that before President Reagan there’s almost no green. And the green, actually, is below the line, which means we ran trade surpluses. But they were small, small enough to ignore for the part of the story up until a much later period, okay, beginning with Reagan.

(c. 28:22) “And, so, what our normal situation was the government ran a deficit and the private sector ran a surplus, which meant the private sector was saving, which is what you would normally expect. It’s sort of a good thing when households spend less than their income. They’re accumulating financial wealth. It helps to get the kids in college and to go into retirement. So, you expect that to be [the case,] normally.

“You could see it as very cyclical. When people get scared, they, actually, save more. When they get really enthusiastic and confident, they spend more. Okay? The two, by identity, had to be equal. The causation is hard to explain. But it largely goes from the private decisions to spend or to save to the budget because if the private sector is scared and not spending, and trying to save, the government had to make up the difference with unemployment compensation and food stamps and reduction of tax revenue to keep the economy going. So, that was the normal case.

(c. 29:30) “The Clinton years, again, are very unusual because the private sector started deficit spending. It’s the other side of the coin. For the government to run a surplus, the private sector needed to run a deficit. Okay?

“And I was at the Levy Institute with Wynne Godley, who was the guy who developed this framework; and the private sector had gone into deficit in 1996. By 1998, we were predicting collapse because the private sector had never done anything like this before. If you look at the blue, the deficit spending by the private sector is really big. For every dollar of income, they were spending $1.06.

(c. 30:08) “In 1998, so, they’d been doing this for two years. They had never done this before. Okay? As far as we know, no country has ever done this before. They’re gonna build up too much debt. They’re gonna get scared and realise, Uh-oh, we can’t service our debt anymore. Some would start going bankrupt. And the others would all cut back spending.

“Well, it went on longer than we thought. But it did happen in 2000. So, in 2000, they stopped spending. Budget went back into deficit, as the economy slowed down. Households retrenched. And you could see there’s a very brief period where they stopped deficit spending. And then the really shocking thing is they started deficit spending again, well, after President Bush came in. They started deficit spending. And that went on for another five years.

“So, for a period of almost ten years, with a brief recession, almost ten years, the private sector spent more than its income, every year. It had never done anything like that before. And, all along, we kept saying: This can’t continue. This is unsustainable. This is going to crash.

“It finally crashed in 2007. We lived through the biggest bubble in human history, not the biggest bubble in United States history, the biggest bubble in human history occurred between 2000 and 2006. It wasn’t just housing. It was also commodities.

So, anyway, finally—I’m spending too much time talking about this picture.

“The foreign sector is the balancing item. So, that when the budget deficit doesn’t equal the private sector surplus, it’s because we are running, either, a trade surplus or a trade deficit.

(c. 32:00) “And, since the years of Ronald Reagan, we have run chronic trade deficits. And, so, that is the green above the line because this shows the capital account surplus for the economy. So, that’s why it’s positive. When we run a current account deficit, we have a capital account surplus. So, that’s the balancing item.

“And the US is in this situation where you have—since we have a current account deficit, even if the private sector balances its budget, we will have a government budget deficit equal to the current account deficit. Okay? It’s the structure of—not just the US economy, but—the global economy, in which, many countries of the world want to sell their stuff to us. We can’t decide, by ourselves, to reduce our current account deficit. It takes two to tango. They have to reduce their desire to export to us in order for us to balance the current account.

“But, anyway, balances balance. It’s a mirror image. If you are saying we want the federal government to balance its budget, in the United States, that has to mean, you want the private sector to deficit spend and run up private debt. You want another boom. That’s what it must mean. Anyone who says we’re going to reduce the government budget deficit down to zero, they’re telling you, we want the private sector to spend again, like it’s 2005—Okay?—and crash again. There’s no other alternative to that, given that—for the foreseeable future, we’re not going to get to a current account surplus. We’re not gonna export more than we import for the foreseeable future. It could change. I don’t know when. I don’t see it happening. I don’t know any economist who is predicting that that’ll happen in the next decade or two.

(c. 34:02) “Okay. It’s claimed that this is unsustainable, even though we’ve been doing it since about 1789. It’s unsustainable. Someday it’s gonna come back and get us—Okay?—these government budget deficits. Someday it’s going to get us. There’s supposed to be this relationship—and this stuff gets wonky—but the basic idea is if the government pays a higher interest rate on its debt, then the growth rate of the economy—mathematically—what happens is the debt ratio tends to grow over time. So, we go from, say, a debt ratio of 40% to GDP to 60% to 100%. Okay? And, as the debt ratio goes up, it means the government has to spend ever more on interest, which makes the debt ratio go up even more.

“And then the bond vigilantes will say, Uh-oh, your government debt ratio is above 60%, or uh-oh, it’s above 100%, or—in the case of Japan—uh-oh, your debt ratio is 200% of GDP—by the way, they still pay 0% interest—200% of GDP—they’re gonna attack you and push your interest rates up, like they did to Greece. So, that’s the basic argument.

(c. 35:17) “So, what we need to show is, first, why a government doesn’t face insolvency, and, so, why there, actually, is no reason to worry about a government default—even if the debt ratio does continue to grow, even if it did.

“And, second, why deficits actually don’t raise interest rates—so, now, unfortunately, we get into the theory part. But just to show you that what I’m going to be arguing is not so far out there, here’s the St. Louis Fed. This is a recent research paper by the St. Louis Fed. The economists here know the St. Louis Fed is a monetarist Fed. It’s a Milton Friedman Fed. Okay? It’s not some crazy bunch of Keynesian type economists. These are monetarist, conservative economists:

“‘As the sole manufacturer of dollars, whose debt is denominated in dollars, the US government can never become insolvent—’

“This is the Fed. Okay.

“‘—unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational. Moreover, there will always be a market for US government debt at home because the US government has the only means of creating risk-free dollar-denominated assets.’

“Now, let me translate to plain English:

“The government can never run out of dollars.

“It can never be forced to default.

“It can never be forced to miss a payment.

“It is never subject to the whims of bond vigilantes.

“This is what the St. Louis Fed tells us. You can find identical statements from Alan Greenspan, from Ben Bernanke. Okay? Again, both monetarists.

“Here, let’s go abroad, Lord Adair Turner, the Chairman of the FSA, he was in line to become the head of the Bank of England. He didn’t get it. But very well respected. He says:

“’Within limits, financing government spending by printing money absolutely, definitively does not lead to inflation.’

“He said:

“‘I accept entirely that this is a very dangerous thing to let out the bag—’

“We don’t wanna tell people this stuff. So, don’t let it get out of this room, right?

“‘—that this is a medicine in small quantities, but a poison in large quantities, but that there exist some circumstances, in which it is appropriate to take that risk.’

“And he’s arguing, this is the time to do it.

“Go back to Paul Samuelson. Maybe some of the older people, that are here, used his textbook, okay, in the 1960s and beyond. He says, ‘I think there’s an’—this is an interview, by the way, with Mark Bowden. [Samuelson] says:

“‘I think there is an element of truth in the superstition that the budget must be balanced at all times.’

“But he goes on later to relax that and say, not even at all times, but over the course of a cycle.

“‘Once it is debunked [that takes away one of the bulwarks that every society must have against expenditure out of control. There must be discipline in the allocation of resources or you will have anarchist chaos and inefficiency.’]

“And then [Samuelson] says:

“‘And one of the functions of old-fashioned religion was to scare people by sometimes what might be regarded as mythsinto behaving in a way that the long-run civilised life requires.’

“So, the necessity of balancing the budget is a myth. It’s a superstition, the equivalent of that old-time religion. So, what is the truth?

(c. 38:31) “If economics is to rise above superstition, you know, I’m a professor, there are professors here—I’m not happy teaching students myths and superstitions. Maybe if you’re selling or marketing something, that’s understandable. But I don’t think it is when you’re an economist.

“So, we have to look at, how does the government actually spend? Ben Bernanke was asked when he was before Congress:

“‘Where did you get all that money you used to bail out Wall Street?Was that tax money?’

“He said:

“‘No, no, no, no, no.’

“He said:

“‘It was keystrokes. We keystroked that money into existence.’

“And that’s absolutely right. That is the way government spends. Spending leads to credits to bank accounts. When the government buys something or makes a Social Security payment, what they do is they keystroke reserves into the account of the bank. And the bank keystrokes into your deposit account. That’s what money is now. It’s keystrokes. Most of it is electronic.

(c. 39:41) “So, the government just credits the bank reserves. And the bank credits the account of the recipients.

“Tax payments are exactly the opposite. They are reverse keystrokes. They lead to debits of accounts. The government debits the bank’s reserves. And the bank debits the account of the taxpayer.

(c. 40:00) “So, if the government keystrokes more credits into existence than it debits, we call that a budget deficit. Okay? It leads to a net credit to banking system reserves and to the accounts of the recipients.

“You can think of money as scorekeeping. Since I’m in America, you all know what this is. [Gesticulating to slide of Fenway Park scoreboard] I was just in Mexico and, fortunately, they all love baseball, too. So, the all immediately recognised. Oh, yes, there we go. Boy, Tampa Bay is beating the socks off of Boston, right?

“You can see the scorekeeper down here in the corner. What if Tampa Bay has another big inning and gets a bunch more runs. Is the scorekeeper ever going to run out of runs to award Tampa Bay? No, he’s not gonna run out. Okay? He’ll just credit it; it’s keystrokes. In the old days, they actually had to physically put the numbers up. Maybe they could’ve run out of ’em. But they can’t anymore. It’s all electronic. They cannot run out of keystrokes.

“If they find out that there was a mistake. The umpire made a bad call or something and he realised he put a run up and they didn’t deserve it. What does he do? It’s a reverse keystroke. Right? He takes it away. Where does it go? It doesn’t go anywhere. He just takes it away.

(c. 41:25) “If what I’m saying is true, if the government keystrokes its spending into existence, why does the government sell bonds? I mean, you can understand why a private firm would sell bonds. They need to borrow. They can’t just keystroke their spending. The federal government keystrokes.

“Okay. Here’s the answer. Deficit spending leads to net credits to banking system reserves. When banks have more reserves than they want, they offer them in the overnight market. In the United States that’s called the Fed Funds Market. If banks, in the aggregate, have more reserves than they want, you have more of them offering reserves in the overnight market than want to borrow them in the overnight market. That pushes the overnight interest rate down.

(c. 42:13) “So—let me repeat this for the people who’ve had some economics because you’re usually taught exactly the opposite, which is wrong. Budget deficits push the interest rate downbecause it leads to excess reserves in the banking system. So, the interest rate is bid down in the overnight market. Budget deficits push the interest rate down.

“The central banks, today, all, even openly, admit that they use interest rate targets. Nobody pretends anymore that they control bank reserves or that they control the money supply. They target the overnight interest rate in the US Fed Funds Rate.

“So, when the Fed sees the excess reserves in the banking system driving the interest rate down, they offer bonds called an open market sale. They sell bonds.

“Banks, that have excess reserves, say, ‘Oh, good. We would rather hold the Treasuries, that pay higher interest.’ Until two years ago, reserves earned zero. So, any interest rate paid on government bonds was better than zero. Bankers aren’t that stupid. Okay?

“So, they would always use the reserves to buy the bonds. So, you can think of bond sales, as being a reserve drain. That’s what they do. They drain reserves banks don’t want out of the banking system. So, bond sales are actually part of the monetary policy.

“The problem is that the Fed, in normal times, has a limited quantity of bonds to sell. They very quickly sell off all the bonds they have in their portfolio. Now, that’s not gonna happen now because, thanks to Uncle Ben, we have quantitative easing, which means the Fed has gone out and bought $2 Trillion dollars worth of bonds. So, they got plenty of ‘em now, but in normal times they didn’t have enough.

(c. 44:07) “So, they call up the Treasury and say, We’re gonna run out of our bonds, if you don’t sell some bonds. So, the Treasury sells bonds, too. Both, the Fed and the Treasury sell bonds. And the functional impact of that is to drain excess reserves out of the system, so the Fed can hit the overnight interest rate target. That’s what it’s all about—interest rate targeting.

“So, you can think of bonds as just an alternative to, either, zero- or low-earning bank reserves. Another way for the markets people is that it increases the duration. What quantitative easing did was decrease the duration of financial assets out in the market.

(c. 44:51) “Now, we do have self-imposed constraints. One of those is the budgeting process, itself. The budgeting process limits the ability of the administration to spend like it’s Weimar all over again. They can only spend what’s been budgeted. So, that is one constraint on government spending.

“Affordability is not a constraint.The government can always afford to spend more, but you don’t want them to. You don’t want ‘em to spend too much for two reasons. They can cause inflation. And, second, if the government is taking resources, it leaves less for the private sector. If the government takes more for the public purpose, there’s less left for the private purpose. So, you wanna constrain the government.

“So, the budgeting process is the way that, you know, all governments do—or, at least, should—constrain themselves. You have to go through budgeting. It’s gotta be approved.

(c. 45:53) “But, in addition to that, the US, Congress, in its infinite wisdom, put on debt limits. Other countries don’t do this. Okay? They say [in the US], Well, we don’t really trust ourselves. We had a budgeting process. But we don’t trust ourselves. So, if we run up against a debt limit, we gotta get together and agree to do it.

“And, as I said, normally that’s not a problem. But today it’s become a political problem.

“In addition, we put on operational constraints. Okay? These didn’t come from nature. And they didn’t—they were not imposed on usby the markets. We decided to do this to ourselves. Okay?

“One [operational constraint]is that we decided, when we created the Fed, that the Treasury would use the Fed as its banker. This was in 1913. Other countries had created central banks, even before 1700. We were really late getting into the game of creating a central bank. Before that the Treasury, either, used private banks or it just spent, itself. It didn’t go through its own government bank. But in 1913, we decided—for a variety of reasons—to create a central bank. And they said, ‘Okay, Treasury, you can only spend if you have your money in the account at the Fed.’ Okay? Alright.

“Then they decided; let’s add one more constraint. ‘And, Treasury, you cannot sell debt to your bank. You can sell it to anybody else. You can’t sell it to your own bank.’

“This would be like you’ve got a bank. Okay? I don’t know, Bank of Portland. That’s where you do your business. Your bank is prohibited from taking your IOU. Any other bank can take it. But your own bank can’t. It’s a very strange limit to put on yourself. But that’s what we decided to do. And a lot of other countries followed us. So, there are countries around the world that do do it this way. They don’t do the debt limit thing, but they do do this. Okay?

(c. 48:02) “And the belief was this would prevent us from becoming Weimar because the Treasury doesn’t have the option of just selling its debt—or we could just simplify this by calling it borrowing—it can’t just borrow from the Fed. The Fed is prohibited from buying Treasuries directly from the Treasury. There are some exceptions to this. It’s not a 100% rule, but it’s pretty close. The Fed can buy bonds, US Treasury bonds, from anybody, except the issuer of US Treasury bonds. The Treasury—another strange thing, if you think about it.

“Okay, so it was believed this would constrain spending because the Treasury could only sell bonds in the private markets, not to the central bank. Now, in fact, it has no impact whatsoever. And the reason is because we set up special banks, called special depositories, that have special kinds of accounts called Tax and Loan Accounts. And these allow the Treasury to completely subvert this operational limit because they can sell the bonds directly to these private banks. And then the private banks sell them on to the Fed. The bonds go right to the Fed, anyway. Okay? And then the Treasury gets its account at the Fed and it can write checks. And, so, it, actually, does not impair the Treasury’s ability to conduct normal business.

(c. 49:33) “Central bank policy—the consensus now is central banks always operate on an overnight interest rate target. That means they always accommodate demand for reserves. And that means they are able to set the overnight interest rate. Now, the Fed does not set all the interest rates. Okay? The Fed sets—directly—the overnight interest rate. They could, if they wanted to, set and hit a target for the interest rate on any maturity of Treasury debt. If they wanted to do it, they can do it directly by buying and selling Treasuries of that maturity in a significant quantity standing ready to always buy or sell at the price consistent with the interest rate that they want to hit. So, they could do that, but they don’t. They set the overnight interest rate. And then the others are set, relative to that one. Okay?

(c. 50:32) “There’s a difference between a country, that has a convertible, versus a non-convertible, currency. You see, a convertible one is where the government says we will convert our currency to a foreign currency on demand at a fixed exchange rate. That’s a convertible currency. Nonconvertible means that they offer you no promise. Now, the United States, we don’t offer any promise. Can you convert the currency? Sure; you can. But you have to do it at whatever exchange rate exists at the time. Okay.

(c. 51:06) “Unlike Greece. Okay? Greece has the most strict kind of convertible currency you possibly can have. They adopted the Euro, which isn’t even their own currency. Okay? So, they are on a very strict convertible standard by adopting, essentially, a foreign currency. It’s a lot like when Argentina adopted the US dollar.

“They can’t control their interest rate.They are subject to the market. A country with a non-convertible currency, like the US and Japan and the UK, we do set our overnight interest rate. It’s not determined in markets.

[slide #27/39] “So, let me summarise. Sovereign currency: Here I mean a country with a government, that issues its own currency. Okay? Now, it can, either, float, manage, or peg its exchange rate—it’s still a sovereign currency, but you give up policy space if you don’t float.

(c. 52:11) “So, I’m going to focus on the ones with more policy space, like the US, Japan, and the UK, where we do float our currencies. In those, then, deficit spending creates private financial wealth. Well, this is true in any of them. It comes from the identities. Note that central bank operations do not—I’ll come back to this in a second—central banks don’t create net wealth. So, the way that I always explain this to my students is, I say: The central bank lends dollars into existence; the Treasury spends dollars into existence. The first one doesn’t create any net financial wealth. The second one does. Budget deficits create private sector surpluses.

(c. 52:56) “It doesn’t matter whether the bonds have to be sold first into the private market first, rather than the Fed, so long as the central bank accommodates reserve demand.

“It doesn’t matter whether the central bank is prohibited from buying new issues because they do it roundabout through the banks. And it doesn’t matter whether Treasury has to have ‘money’ in its account at the central bank to spend because the central bank and banks cooperate to make sure the Treasury always has that.

“All of this has been describing the system we have. It’s not a recommendation. Okay? We can add on to this understanding what Abba Lerner—a famous economist,who, actually, spent some time teaching at the University of Missouri-KansasCity, where I’m from—said:

“‘A government should spend more, if there is unemployment.’

“How can you tell if the government is spending enough? Or not enough? Or too much? Look at employment. You don’t look at the size of the budget deficit. He said:

“‘You look at whether you have unemployment. If you have unemployment, you’re not spending enough. If you’re at full employment, you shouldn’t increase spending anymore.’ Okay? That’s when you know when you’ve spent enough. You’ve got full employment.

(c. 54:07) “The second principle of functional finance is the government should supply more money—he meant bank reserves—if the interest rate is too high. Again, you can’t tell by the quantity of reserves out there. You [can] tell by looking at the interest rate.

“So, in other words, what he’s saying is you don’t worry about the budgetary outcome. The debt outcome should never be a primary consideration of spending.

[Slide #29/39] “Continuing on with policy. These are long quotes. I’ll read ‘em very quickly. The first one is by Milton Friedman. He said:

“‘Let’s suppose that one day a helicopter flies over this community and drops an additional $1000 in bills from the sky, which is, [of course, hastily] collected [by members of the community]’ and then spent.

“This is, of course, Milton Friedman’s famous quote, which everyone interprets as saying; monetary policy is like helicopters flying around dropping money.And that’s inflationary. Okay? That was his argument.

(c. 55:00) “Here is Keynes. Keynes says, and many of you will recognise this quote, too:

“‘If the Treasury were to—he’s talking about in conditions of a depression or deep recession, like we’re in now.

“‘If the Treasury were to fill old bottles with bank notes, bury them at suitable depths in disused coal mines…and leave it to private enterprise [on tried principles of laissez faire]’ to hire workers ‘to dig [the notes up again…’], we’d solve the unemployment problem.

“Now, it wasn’t that he was recommending that this is the best policy. This was supposed to be ironic. He was saying, look, if policy makers are too stupid to think of better uses for the labour, at least you could dig holes and bury money. Okay? Obviously, there are better solutions, but he was saying that if you did this, then ‘the real income of the country will be a good deal greater than it actually is.’ And you could get yourself out of a depression by doing something like this.

[Slide #30/39] (c. 55:55) “Here is Martin Wolf today, probably, you read him in the Financial Times. He’s one of the great journalists today. He said:

“‘In the present exceptional circumstances, when expanding private credit and spending is so hard, if not downright dangerous—’

“You know, the idea that we should get banks lending again to the private sector, so that they could deficit spend again is fairly crazy.

“‘The case for using the state’s power to create credit and money in support of public spending is strong.’

“‘Japan should have done some outright monetary financing—’

“He means deficit spending.

“‘—over the last 20 years, and if it had done so, would now have a higher nominal [gross domestic product], some combination of a higher price level—’

“That might sound scary, but Japan would love to have inflation. They’ve got deflation. Okay?

“‘—[and a higher real output level], and a lower debt to [gross domestic product] ratio.’

“If they had deficit spent more in the past, their debt ratio today would, actually, be lower. Their debt ration now is 200% of GDP because their economy is still in the tank. If they had been able to get growth going the debt ratio would be lower than it is now.

[Slide #31/39] (c. 57:09) “Is Japan a scary precedent? Possibly. Japan, in the 1980s, like us in the 2000s, was growing rapidly. And, at the time, everyone in America pointed to Japan as the path we should be following, not recognising that the government deficit was helping them to grow. But the problem was that they had a tremendous real estate bubble in commercial real estate, mostly, not like in the US, where it, largely, in the 2000s, was residential real estate.

“Anyway, then the government budget moved to a surplus and it started sucking income out of the economy. And the economy collapsed. And they’ve had 20 years of recession, deflation, and falling real estate prices. And how did they respond to that? With quantitative easing, just like we’ve done, very low interest rate policy.

[Slide #32/39] “So, just mapping US data so far onto Japanese data over the past 20 years, it does look scarily similar. Here’s inflation data, CPI data for Japan. And you could see Japan has been, actually, below zero for years now. That is deflation.

[Slide #33/39] “Here is the budget deficit, as a percent of GDP. Their budget deficit went to 10% of GDP and then started declining, just as ours is doing.

[Slide #34/39] “And here is their interest rate policy. They took a little longer to get to zero than we did. We went to zero quicker. And they’ve been at zero forever. And they’re still stuck. Okay? We’re trying the same thing that they tried to get out of their doldrums and with pretty much the same results, so far. They tried some very small fiscal stimulus packages, but, then, they always worried about the budget deficit. And they tightened again, usually, with a tax increase. And, so, they’ve been stuck in this recession for a very long time.

(c. 59:20) “Let me just finish up now. I just wanna point out, because people say we could be like Greece, the Euro nations are very different from us. The member states all gave up their own currencies when they joined the euro. So, Italy gave up the lira. They adopted what is, essentially, a foreign currency—called the euro. And they became very much like a USA state. They became a user of the currency. Okay? Oregon is a user of the dollar. The state of Oregon is not the issuer of the dollar. In fact, if they tried printing it up, I think Uncle Sam will be here pretty quick and tell you that you cannot do that.

“So, they became much like the US states. They’re constrained in their spending by their tax revenue, their bond sales in the markets, and the willingness of the ECB to lend. Their problem, unlike Oregon, is they have no Uncle Sam. They do have a central bank, which says every federal reserve district, which (very brilliantly) is not identical to state boundaries—that, actually, was a good set up—there still is the possibility that the reserve bank of San Francisco can go to the Fed, just as their reserve bank can go to the ECB. But they don’t have an Uncle Sam to look out for them.

(c. 1:00:00) “When the Euro was first set up, we did the analysis this way. We said, ‘Ah, okay. Italy has become the new New Jersey. Or France has become the new New York. Hey, you know what? US states go bankrupt, now and then. That can happen to them, too.’ We thought, the first time there was a crisis, a financial crisis in Euroland, the euro governments would immediately get into trouble. And that’s exactly what happened.

“By adopting the euro, the sovereign nations turned into something like US states. Unlike US states, the euro governments have to fund their pensions, their health care, and they have to bail out their banking systems. And that last one is what killed them.

“If you looked at US states before the crisis hit, they had debt ratios you could see in the teens. Okay? Does anyone remember—how big of a debt ratio was permitted under Maastricht? 60%. Okay. So, Maastricht criteria said, Greece, Italy, and so on, go ahead, you can run up debt ratios to 60%. When we found the data on US states, we said, No, you can’t. You run a debt ratio bigger than 15% and the market’s gonna shut you down.‘ Okay?

“And, so, it was very obvious that the 60% was way too high for a non-sovereign government. So, a crisis was going to kill them.

“Okay, conclusions:

“Currency-issuing government spends by crediting bank accounts.

“Taxing by debiting can always afford to spend more.

“There are issues. Inflation is an issue. You have to worry about inflation.

“Exchange rate effects: the dollar could go down, if we spend more. That could happen.

“And there could possibly be interest rate effects, not on the overnight, on the other longer maturity rates.

“A sovereign currency gives more policy space.

“There’s no default risk.

“You can control your interest rates.

“You can use policy to achieve full employment.

“Now, I wanna close by telling you what I did’t say because a lot of times people hear things I didn’t say. So,let’s make it clear what I didn’t say:

“I did say a sovereign government faces no financial constraints. It cannot become insolvent in its own non-convertible currency. But it can only buy what’s for sale in its own currency. Not a problem in the US. Anything, for sale for dollars, anything for sale in the United States is for sale in dollars and the US government can buy it. You go to some developing countries, there are things, that are not for sale in the local currency. Then, the government cannot buy them in its local currency. Okay? But not an issue for developed countries.

“I did not say the government ought to buy everything for sale. Okay? The size of the government is a political decision with economic effects—mostly it’s a political decision. Capitalist economies seem to work okay with governments, that are about 20% of GDP—the US, Japan isn’t much bigger. And some capitalist countries work very well with governments, that are 50% of GDP—France.

“So, somewhere in that range is probably where you need to be—20 to 50%. What do you choose? Politics. It depends on what you want, what you want your government to provide.

“I did not say deficits can’t be inflationary.

“Deficits, that are too big canbe inflationary.

“And I did not say that deficits cannot affect exchange rates. That’s why you need a floating currency, so that you don’t have to worry about the pressure of holding an exchange rate when you are stimulating your own economy. That’s it.

“Thanks. [Applause]”

Question and Answer

Host: “We have about 25 minutes for questions.”

Questioner #1: “Is there any reason to believe that there is—”

***

Transcript by Felipe Messina for Media Roots, Breaking the Set, and New Economic Perspectives

MEDIA ROOTS — The deceptive term “sequester” in Obamaspeak refers to social spending cuts looming, ostensibly, in order to “balance the budget,” as if the US federal budget were the same as a household budget in need of balancing. The big mistake the public makes, aided by a lying corporate media perpetuating myths about the US economy, is it falls for the fallacious argument the federal government, a sovereign currency issuer of the US dollar, needs to “balance its budget.”

What happens is the federal budget (domestic public sector) is viewed in isolation, out of context, isolated from the foreign sector and the domestic private sector. This renders popular analysis of the federal budget flawed. So, of course Obama perpetuates existing myths about our monetary system, because he’s funded by Wall Street. UMKC Professor William K. Black breaks it down precisely how Obama fakes the funk.

Messina

***

NEW ECONOMIC PERSPECTIVES — We are in the midst of the blame game about the “Sequester.” I wrote last year about the fact that President Obama had twice blocked Republican efforts to remove the Sequester. President Obama went so far as to issue a veto threat to block the second effort. I found contemporaneous reportage on the President’s efforts to preserve the Sequester – and the articles were not critical of those efforts. I found no contemporaneous rebuttal by the administration of these reports.

In fairness, the Republicans did “start it” by threatening to cause the U.S. to default on its debts in 2011. Their actions were grotesquely irresponsible and anti-American. It is also true that the Republicans often supported the Sequester.

The point I was making was not who should be blamed for the insanity of the Sequester. The answer was always both political parties. I raised the President’s efforts to save the Sequester because they revealed his real preferences. Those of us who teach economics explain to our students that what people say about their preferences is not as reliable as how they act. Their actions reveal their true preferences. President Obama has always known that the Sequester is terrible public policy. He has blasted it as a “manufactured crisis.”

The administration has stated publicly the three reasons this is so. First, the Sequester represents self-destructive austerity. Indeed, it would be the fourth act of self-destructive austerity. The August 2011 budget deal already sharply limited spending and the January 2013 “fiscal cliff” deal raised taxes on the wealthiest Americans and restored the full payroll tax. The cumulative effect of these three forms of austerity has already strangled the (modest) recovery – adding the Sequester, particularly given the Eurozone’s austerity-induced recession, could tip us into a gratuitous recession.

Second, the Sequester is a particularly stupid way to inflict austerity on a Nation. It is a bad combination of across the board cuts – but with many exemptions that lead to the cuts concentrating heavily in many vital programs that are already badly underfunded.

Third, conservatives purport to believe in what Paul Krugman derisively calls the “confidence fairy.” They assert that uncertainty explains our inadequate demand. The absurd, self-destructive austerity deals induced or threatened by the Sequester have caused recurrent crises and maximized uncertainty. They also show that the U.S. is not ready for prime time.

When he acted to save the Sequester, Obama proved that he preferred the Sequester to the alternative. When the alternative threatened by the Republicans was causing a default on the U.S. debt (by refusing to increase the debt limit), one could understand Obama’s preference (though even there I would have called the Republican bluff). The Republicans, however, had extended the debt limit in both of the cases that President Obama acted to save the Sequester in 2011.

Similarly, President Obama has revealed his real preferences in the current blame game by not calling for a clean bill eliminating the Sequester. It is striking that as far as I know (1) neither Obama nor any administration official has called for the elimination of the Sequester and (2) we have a fairly silly blame game about how the Sequester was created without discussing the implications of Obama’s continuing failure to call for the elimination of the Sequester despite his knowledge that it is highly self-destructive.

The only logical inference that can be drawn is that Obama remains committed to inflicting the “Grand Bargain” (really, the Grand Betrayal) on the Nation in his quest for a “legacy” and continues to believe that the Sequester provides him the essential leverage he feels he needs to coerce Senate progressives to adopt austerity, make deep cuts in vital social programs, and to begin to unravel the safety net. Obama’s newest budget offer includes cuts to the safety net and provides that 2/3 of the austerity inflicted would consist of spending cuts instead of tax increases. When that package is one’s starting position the end result of any deal will be far worse.

In any event, there is a clear answer to how to help our Nation. Both Parties should agree tomorrow to do a clean deal eliminating the Sequester without any conditions. By doing so, Obama would demonstrate that he had no desire to inflict the Grand Betrayal.

***

UPDATED 1 MAR 2013 12:39 (CST):

NEW ECONOMIC PERSPECTIVES — We have been strangling the economic recovery through economic incompetence – and worse is in store because President Obama continues to embrace (1) the self-inflicted wound of austerity, (2) austerity primarily through cuts in vital social programs that are already under-funded, and (3) attacking the safety net by reducing Social Security and Medicare benefits. The latest insanity is the Sequester – the fourth act of austerity in the last 20 months. The August 2011 budget deal caused large cuts to social spending. The January 2013 “fiscal cliff” deal increased taxes on the wealthy and ended the moratorium on collecting the full payroll tax. The Sequester will be the fourth assault on our already weak economic recovery. We have a jobs crisis in America – not a government spending crisis and the cumulative effect of these four acts of austerity has caused a certainty of weak growth and a serious risk that we will throw our economy back into recession. The Eurozone’s recession – caused by austerity – greatly adds to the risk to our economy because Europe remains our leading trading partner.

President Obama and a host of administration spokespersons have condemned the Sequestration, explaining how it will cause catastrophic damage to hundreds of vital government services. Those of us who teach economics, however, always stress “revealed preferences” – it’s not what you say that matters, it’s what you do that matters. Obama has revealed his preference by refusing to sponsor, or even support, a clean bill that would kill the sequestration threat to our Nation. Instead, he has nominated Jacob Lew, the author of the Sequestration provision, as his principal economic advisor. Lew is one of the strongest proponents of austerity and what he and Obama call the “Grand Bargain” – which would inflict large cuts in social programs and the safety net and some increases in revenues. Obama has made clear that he hopes this Grand Betrayal (my phrase) will be his legacy. Obama and Lew do not want to remove the Sequester because they view it as creating the leverage – over progressives – essential to induce them to vote for the Grand Betrayal.

Further evidence of Obama’s continuing support for the Sequester was revealed in an odd fashion today. Bob Woodward is in a controversy because of his column about Sequestration. His column made two primary points. First, the administration authored the Sequester. Second, Woodward claimed that Obama was “moving the goal posts” by asking for revenue increases. Woodward was criticized by many Democrats for this column and created a further controversy by saying that the administration threatened him. It turned out that the purported threat was based on a statement by Gene Sperling, Obama’s economics advisor. David Weigel’s column summarizes the dispute.

Weigel comes out where I do on each of the three issues. Yes, the administration created the Sequester and has fought to keep it alive when Republicans tried to kill it. (The Republicans “started it” by their obscene extortion in 2011 in which they threatened to force a default.) No, Obama has not moved the goal posts. No, Sperling did not “threaten” Woodward. I raise this background simply to provide a context for Sperling’s comments about the reasons that the administration created and continues to support the Sequester.

“The idea that the sequester was to force both sides to go back to try at a big or grand bar[g]ain with a mix of entitlements and revenues (even if there were serious disagreements on composition) was part of the DNA of the thing from the start. It was an accepted part of the understanding — from the start. Really.”

There may have been big disagreements over rates and ratios — but that it was supposed to be replaced by entitlements and revenues of some form is not controversial. (Indeed, the discretionary savings amount from the Boehner-Obama negotiations were locked in in BCA [Budget Control Act of 2011]: the sequester was just designed to force all back to table on entitlements and revenues.)

Obama continues to want to “force” a “grand bargain” in which he proposes to make large cuts to social programs, some tax increases, and reductions in the safety net. Again, Obama can easily break with this strategy of choking our economic recovery by supporting a clean bill that would kill the Sequester instead of our economy.

MEDIA ROOTS – Recently on Breaking the Set, Abby Martin had the opportunity to interview the Libertarian Party’s Presidential candidate, Governor Gary Johnson, the Green Party’s Presidential candidate, Dr. Jill Stein and the Party for Socialism and Liberation’s candidate for President, Peta Lindsay. Stein and Johnson are the primary “third-party” candidates in this year’s election, yet they have been completely shut out from the Presidential debates.

Dr. Stein made recent independent news headlines after being arrested outside the last presidential debates when attempting to enter without the proper “credentials.” More recently, Gov. Johnson is involved in a lawsuit he filed last week against the Commission on Presidential Debates for denying access to the final debate in Florida.

At this year’s Republic National Convention in Tampa, Media Roots also had the opportunity to catch up with Rocky Anderson, Presidential candidate for the Justice Party. He is emphatic that America must return to an era of “broad-based democracy” in order for the country to regain its former glory and provided three specific items that the federal government must do now to get back on track. Mr. Anderson also discusses the “mallification” of America, voter suppression, and the differences between himself and Dr. Ron Paul.

Peta Lindsay, the candidate of the Party for Socialism and Liberation Party, is originally from Washington DC and is now pursuing a masters in public education at USC. She suggests that America re-organize its society with socialist governance, and outlines her vision in the interview below.

Constitutionalist Party nominee and former Congressman Virgil Goode, appears to only have a significant following in the contested swing state of Virginia, where he served for twelve years first as a Democrat, then Independent, and finally as a Republican.

The two-party system that has been dominating the American political landscape for most of its history. It seems now that this facade is crumbling at an increasing rate with voters learning more about who else is running and for which values they stand. For the most part, the entire two-party 2012 Presidential race has been a scripted charade. However, history could be made as it may be the last of its kind for the political duopoly may not last to see another election season.

Oskar Mosco for Media Roots

***

Dr. Jill Stein discusses the “Green New Deal” and breaking the “lesser of two evils” mentality

Gov. Gary Johnson discusses how to fix the two-tiered corporatocracy and his vision for America.

Peta Lindsay, PSL (Party for Socialism and Liberation) talks about the socialist vision for America.

Former mayor of Salt Lake City, Rocky Anderson, discusses with Media Roots’ Adam Miezo

his idea for how to restore a democratic society in the United States.

MEDIA ROOTS — “Both parties have conspired to bring us disaster,” says Professor William K. Black, a leading white collar criminologist, who also teaches economics and law at the University of Missouri-Kansas City. “This has strangled the recovery and may even put the economy back into recession.” Professor Black gives a crucial recap of Obama’s (and both Democrats’ and Republicans’) recent history of assaults against the working-class, also known as austerity.

MEDIA ROOTS — “Both parties have conspired to bring us disaster,” says Professor William K. Black, a leading white collar criminologist, who also teaches economics and law at the University of Missouri-Kansas City. “This has strangled the recovery and may even put the economy back into recession.” Professor Black gives a crucial recap of Obama’s (and both Democrats’ and Republicans’) recent history of assaults against the working-class, also known as austerity. MEDIA ROOTS — Obama’s attacks on the social safety net continue, fueled by the claim the USA is running out of dollars. During the recent Steinhardt Lecture at Lewis & Clark College in Oregon, UMKC Professor L. Randall Wray debunked various economic myths marketed in today’s headlines, which are enforced in universities and echoed by the Obama Administration. These same myths provide pretexts for “fiscal austerity” and “