MEDIA ROOTS —Media Roots contributor Chris Musgrave documented and edited inspiring and moving footage in the Downtown and Fruitvale areas of Oakland to capture the festive and optimistic spirit of engaged citizenry petitioning their government for a redress of grievances on May Day, May 1, 2012, under the universal banner of the Occupy Movement and in solidarity with immigrant and non-immigrant workers—under-, unemployed, employed, organised, or otherwise—and their need for improved wages and working conditions. The decision was, apparently, made by regional Occupy General Assemblies to stand in support with labour picket lines, rather than attempt to shut down the Golden Gate Bridge, reflecting an increasing working-class consciousness among the northern California Occupy Movement.

While the event was mostly peaceful, the isolated instances of property damage were magnified by most media outlets, including public media. Also, standards of criminalising demonstrators seemed to be worsening, as even chalk writing, an activity children on my street engage in everyday, was being criminalised. And, of course, once the sun set and many were unable to continue demonstrating, Oakland police, alongside multiple police agencies began firing tear gas and taking other repressive measures to stamp out remaining demonstrators.

Messina

***

***

UPDATE (4 MAY 2012 17:55 PDT):

KPFA/PACIFICA RADIO — “Again, May Day actions have begun around the world, around the nation, and in California [today May, 1, 2012]. And in a little bit we’ll be checking in to Los Angeles. But, of course, all eyes were also, today, on San Francisco and what was gonna happen with the Golden Gate Bridge. There were previous reports about trying to shut the bridge down over the weekend. The unions said they did not want that to happen. The union is in contract dispute and trying to get contract for their workers with the Golden Gate employers. But they said, at the last moment, not to shut down the Bridge, but instead to hold a major picket.

(c. 12:31) “Apparently, or reportedly, the Ferries have been shut down. And we have this report from Pacifica correspondent John Hamilton from the San Francisco Ferry Building.”

“[Brass Liberation Orchestra plays] As the Brass Liberation Orchestra provided a soundtrack, about a hundred striking Golden Gate Ferry workers and their supporters picketed at San Francisco’s iconic Ferry Building this morning [May, 2012]. Notably, absent was the usual hustle and bustle at the Ferry terminal where boats operated by the Golden Gate Bridge Highway and Transportation District.

“[Sounds of Demonstrators’ Call and Response Chanting] Get back! (Get Back!) Go away! (Go Away!) Fight Back! (Fight Back!)”

(c. 13:10) “All service on the Ferries, which normally shuttle thousands of commuters and tourists from Larkspur and Sausalito to and from San Francisco, has been shut down until 2:15 this afternoon [May 1, 2012] in response to the strike.

Michael Villeggiante (c. 13:30): “They’re on strike. They’re trying to negotiate their healthcare plan. And they’re not negotiating in good faith. The deal that they have on the table is outrageously high for the working-class persons. They’ve already given concessions. And that they’re in the middle of trying to get what they need. And this is just a show of solidarity with the workers that they need to come to the table and bargain and make the deal.”

John Hamilton (c. 13:57): “[Demonstrators and Picketers Chanting] The Inlandboatmen’s Union is just one of several unions comprising the Golden Gate Labor Coalition, whose workers have gone since July without a contract. The Golden Gate Bridge District wants to force workers to pay up to 8% of their salary to cover health benefits, which are now provided free of charge. Robert Irminger is Strike Captain of today’s picket line in San Francisco.”

Robert Irminger (c. 14:23): “The workers, that are on strike today are the terminal assistants who work in these terminals, they’re jobs are up for elimination. The Bridge District last year eliminated Ticket Sellers, which has created mass confusion for, particularly, tourists trying to buy tickets from machines. And now they’re trying to do the same with the people in the terminal, who help maintain the terminal and also answer the questions for the tourists. So, that is the immediate reason we have a strike. And, of course, when those brothers put up a picket line, the other bargaining units on the Ferry boats as well as the captains belong to the Marine Engineers’ Beneficial Association wouldn’t cross those picket lines.”

John Hamilton (c. 15:05): “The IBU and its sister unions had initially planned an informational picket this May Day at the Golden Gate Bridge, but shifted the pickets to Ferry terminals with today’s strike. The Golden Gate Labor Coalition convinced members of the Occupy Movement to call off plans to shut down the Golden Gate Bridge and to, instead, join picket lines. Clarence Thomas is a Member and former Officer with ILWU Local 10, representing longshore and warehouse workers in the [S.F.] Bay Area. He’s also active in the Occupy Oakland Movement.”

Clarence Thomas (c. 15:34): “It’s very, very important that we take these actions today, International Workers’ Day, because this is the day, that celebrates the struggle for the eight-hour workday in this country. It’s also a day, that celebrates worker independence. Workers need to be independent. They need to be able to organise, mobilise in their own name. And they need to be able to use direct action and general strike in order to gain victory.”

John Hamilton (c. 16:00): “Now, the Occupy Movement, which you’ve been a part of in the Bay Area, had initially called to shut down the Golden Gate Bridge today. And then it changed its plans to join an informational picket when requested by the union coalition representing all the Golden Gate Bridge workers. And then that call was since changed to here.

“I do know that there was some frustration within the Occupy Movement that the large signature action was no longer going to occur today. Your thoughts on that dynamic.”

Clarence Thomas (c. 16:25): “Well, I’m like you. I just found out that there was not going to be an action on the Golden Gate Bridge last night. I don’t want to speculate, as to why that happened. But I do want to say this: The whole idea for reclaiming the history and tradition of May Day has not come from the labour bureaucracy. It’s come from the rank and file. And I would imagine that the rank and file was really the segment of the union that was really interested in taking this direct action at the Golden Gate Bridge. I would not imagine that the labour bureaucracy would have been in favour of that. And I say that because historically there’s been a great deal of influence of the Democrat Party over labour. And I believe that when we talk about taking this kind of action, this kind of direct action, it’s coming from the rank and file because the rank and file is getting pretty tired of what’s going on with labour.

(c. 17:20) “Labour in the private sector is only represented by 7% of the workforce. That’s the lowest since 1900. So, the rank and file wants to see much more direct action.The rank and file wants to see strikes when appropriate. And, as a matter of fact, that is the reason the California Nurse’s Association are going out [to strike]—4,500 nurses at nine different Sutter hospitals are going out on strike. And they will be out on strike for five days.

“So, I think that sort of like gives you some indication of what’s going on in the labour movement, in my opinion. I’m not speaking for the [ILWU] Local [10]. These are my own thoughts.”

John Hamilton (c. 18:03): “Meanwhile, there are May Day actions across San Francisco today, including a 10am immigrants’ rights march underway in the Mission District and plans for a march to Occupy the Financial District and public sector workers, with SEIU Local 1021, plan a rally against downtown greed inside City Hall today until quote ‘they kick us out.’

“Reporting from Downtown San Francisco, I’m John Hamilton, Pacifica Radio, KPFA.”

Transcript by Felipe Messina for Media Roots and KPFA/Pacifica Radio

Pacifica Radio’s Guns and Butter has stayed on the drumbeat coverage of the revolutionary economic school of thought, Modern Monetary Theory (MMT), broadcasting extensive audio from the grassroots economic summit in Rimini, Italy produced by journalist Paolo Barnard: Summit Modern Money Theory 2012. At Media Roots, we’ve covered the entire series. With this week’s instalment, Dr. Stephanie Kelton’s discussion includes:

“Myths about taxation and government revenues in a sovereign currency situation; debts and deficits; full social security and price stability; the use of sectoral balances to analyze the financial position of the different sectors of the macro economy; the three sectors of the macro economy; the two rules governing the three sectors; the financial balance model.”

Messina

***

GUNS AND BUTTER — “MMT emphasises the relationship between the state’s power over its money and its power to do things, real things, to conduct policy in an unconstrained way. It emphasises that the state, because of its power over money, has a form of power to command resources in the economy.” —Dr. Stephanie Kelton

“I’m Bonnie Faulkner. Today on Guns and Butter: Stephanie Kelton. Today’s show: Modern Money Theory Explained.

“Today’s presentation was given at the first Italian grassroots economic summit on Modern Money Theory in Rimini, Italy in February, 2012.

“Stephanie Kelton is associate professor of economics at the University of Missouri, Kansas City, research scholar at the Levy Economics Institute, and director of graduate student research at the Center for Full Employment and Price Stability.”

Dr. Stephanie Kelton (c. 1:45): “I’m going to cover some new ground. And I’m also gonna go back and talk a little bit about a few really important concepts in MMT, that Paolo [Barnard] asked me to spend some more time talking about because I, maybe, went a little bit too quickly in one of the previous lessons. So, let’s talk about MMT. And why we think it’s such a revolutionary way to think about so many important economic questions.

“A day ago, two days ago, I forget, I’ve been awake a long time. The Financial Times ran an article on MMT. It was a big deal for us in terms of getting these ideas out there, into the mainstream and taken seriously by politicians, financial writers, and journalists, academics, and even into the hands of regular people, who pick up and read the papers. (c. 2:53) “The Financial Times piece said that seeing MMT is like seeing an autostereogram, those images that look wavy and like there’s no picture. But if you let your eyes rest long enough, the picture becomes clear. And this is how the Financial Times described MMT. Some people might see it right away. And others will have to spend more time wrestling in their minds with some of the ideas because they’re so counter to everything, that we’ve been taught and that we thought we understood about money and government deficits and debt.

(c. 3:39) “And, so, I wanna go back and talk again about some of those important concepts. We think, most people think, that the government collects taxes from us. And raises money by selling bonds, so that it can finance its expenditures: ‘The government needs our money, in order to spend.’ But MMT rejects that. MMT says that a sovereign currency issuer doesn’t have to go out and get the currency from the users in the economy. The sovereign currency spends its own IOUs, it spends its own money. It creates its own currency.

(c. 4:32) “Not only that, but the taxes they collect from us can’t actually finance anything. And the bonds, that are sold to raise revenue for the state, in a sovereign government, also doesn’t pay for government spending.

“We think of two aspects of monetary channels. We think of a vertical channel; this is where state money becomes important. MMT emphasises that the state spends by issuing, what we call, high-powered money. High-powered money is a fancy word for the currency of the state, the notes, the coins, and also the liabilities of the central bank, that are called bank reserves.

(c. 5:27) “When you and I write a check to the government to pay our taxes, the check goes through a process where our bank account gets debited; and the numbers go down. A government account gets a credit; and the numbers go up. But the money supply, the high-powered money itself, the liabilities of the state aredestroyed in the process. They are eliminated from balance sheets. The money has gone down the drain and it can’t be used to finance anything.

(c. 6:07) “In addition to the vertical money—the state money—there is a horizontal aspect in any modern monetary system. Most of the transactions in the private sector don’t involve the government, but private-issued credit money. We can think of this as the leveraging of state money. So, high-powered money is the liability of the government. It sits at the top of the pyramid. And the private sector uses the government’s money to leverage the creation of its own IOUs, its own money, its own debt.

(c. 6:58) “In all modern systems, the central bank targets an overnight interest rate. And then it supplies reserves, on demand, horizontally, at the interest rate, that it sets. It also drains any excess reserves using what we call open market operations, buying and selling government bonds to hit its overnight interest rate target. So, bonds are thought of, more appropriately, not as a financing tool, but as an instrument of monetary policy. Bonds help the government coordinate the reserve add, that is caused by its government spending, with the reserve drain, that’s caused by the collection of taxes.

“In the US, the Treasuryand the Fedhave a very complex way of coordinating the government’s fiscal operations. Many of us in the MMT school have written about this. It is very complex. It involves a lot of institutional detail and it isn’t something, that we need to cover here today. If you’re interested in finding out how the very detailed operations work, you can look for something published by Scott Fullwileron the New Economic Perspectives blog. You can look back at an article I published in 2000, in the Journal of Economic Issues, that was called ‘Do Taxes and Bonds Finance Government Spending?‘

(c. 8:52) “And, of course, Randy Wray’sbook, Understanding Modern Money, also deals with some of this. But I’m gonna skip over the operational details and just tell you that when government spends it adds new money to the banking system. When government collects taxes, it takes money out of the banking system. If the government spends more than it takes out, we say that the government has run a deficit. The deficit leaves extra reserves in the banking system. And this triggers a response by the central bank. The extra reserves push the interest rate down. This is different from what conventional economics teaches us. Conventional economics teaches that a government deficit should push interest rates up because the government is thought to compete for some limited pool of savings, and if you want to increase your deficit, you have to pay a higher price to get some of those savings. MMT rejects that.

“We understand that the state creates money, that money is not scarce, that the government doesn’t borrow household saving to finance its deficit, but rather spends first, creating the reserves, that it then drains by selling bonds. So, the private sector loses the reserves and gains the government bonds. This is how bonds are used to maintain interest rates in a sovereign currency setting.

“We use a graph. I don’t know how helpful it is. But the vertical component, is this component, that goes straight up and down, and it shows that Treasury spending adds high-powered money (HPM), that builds up in banks until we pay taxes and then some of that money goes down the drain or banks use the state money to create their own liabilities, lending to private citizens and to private firms, leveraging the state’s money.

(c. 11:31) “So, this is what we like to think of as the vertical and horizontal parts of the story in MMT. It incorporates the credit theory of money, endogenous money theory, and state money. It’s all related to Lerner’s Theory of Functional Finance. In that piece that Lerner wrote, entitled ‘Functional Finance and the Federal Debt,’ Lerner explained that taxes don’t finance anything. The government can’t spend the money it collects. It’s eliminated. And he understood that bond sales are a tool for conducting monetary policy. Conventional economics teaches that bonds are a tool for fiscal policy, that they are financing tools. MMT views that very differently. The bonds are important because they allow the central bank to sell and buy bonds, adding and draining reserves from the banking system in order to hit its interest rate target.

(c. 12:44) “So, we should reject the orthodox theory because it’s wrong. Conventional wisdom on government finance, taxes, and bonds is incorrect. The conventional theory is that if the government were to finance its spending by creating new money that it would be inflationary, hyperinflationary, they usually say. But, in fact, as MMT shows, all government spending is, by definition, financed by the creation of new money. Sometimes, people think that we’re proposing that government do something different, that MMT says sovereign governments should finance their spending by creating new money. We’re just describing the way they do it now. So, this isn’t a policy proposal. It isn’t going to lead to inflation because they already do it that way and it’s not inflationary.

(c. 13:52) “The orthodox position again suggests that the government sells bonds and that they have to compete for some little, limited, pool of financial resource that’s out there, and if the government wants a piece of that pool and private firms want a piece and households want a piece, we have to outbid one another, and the price of those savings goes up. The argument in the textbooks is that as the price goes up, the interest rate rises, that this crowds out other forms of spending. The government comes in and sees that pool and says I want this piece, pushes the interest rate up for all of the other borrowers who want to borrow.

(c. 14:43) “And, so, it crowds out the more efficient kinds of private sector spending to make room for the inefficient big government spending. This is the conventional story. But, of course, this is wrong. The bonds are sold in order to take back government money that was created by running the government deficit in the first place. So, the deficit creates the money that is then made available for purchasing the bonds. The pool of resources is not limited. It grows with deficit spending.

“So, everything that the conventional story teaches, what students in any economics class, in any classroom—as we were told yesterday, in Italy they’re being exposed to an orthodox, neoclassical version of economics that doesn’t apply to governments that issue a sovereign currency.”

Bonnie Faulkner (c. 15:54): “You’re listening to professor and research scholar, Stephanie Kelton. Today’s show: ‘Modern Money Theory Explained.’ I’m Bonnie Faulkner. This is Guns and Butter.

Dr. Stephanie Kelton: “MMT emphasises the relationship between the state’s power over its money and its power to do things, real things, to conduct policy in an unconstrained way. It emphasises that the state, because of its power over money, has a form of power to command resources in the economy. The state imposes the tax; that allows the state to get people to want to work and produce and provide things to the state in order to get the money that they need to settle the tax liability. This way, the state has command over how to use society’s resources. It’s not something that’s immediately obvious, but it’s central to MMT.

(c. 17:06) “And, so, at an event like this, what we want to do, as much as anything, is to lift that veil that conceals the potential that the state has to use the monetary system in the public interest. [Applause]

“We talked a little bit yesterday about how economists think about the problem of unemployment. Essentially, there are three options when it comes to dealing with the inevitability of unemployment in any market economy. Pure unemployment means that the unemployed sit idle, as a buffer stock of people—human beings—who get no wage and have nothing useful to do. They are assigned no tasks and they have no income.

“Under most systems, there is some form of support for the unemployed, a safety net of some kind. It might be unemployment compensation, a small payment made to the person who’s lost a job and can’t find one. That payment might go on for a period of weeks, months, or even years. All the while, the person is drawing an income, but has no tasks to perform.

“The third option, the one that MMT prefers, is a buffer stock of, not, unemployed, but of employed people. And I talked about this yesterday and we referred to it as an Employer of Last Resort [ELR] programme or a Job Guarantee. In a programme like this, when a person loses a job in the private sector or in the public sector, they have another job to go to. The government does not allow them to sit idle and to pay them to do nothing. It assigns them a useful task, something society needs done. They get a wage. And they get a task.

“We mentioned yesterday that Argentinaimplemented a form of a Job Guarantee, theirs was called the Jefes Programme. It offered a job to the head of household. It gave them a useful task and it paid them a basic wage. It was highly successful.

“ELR provides people with a transition job, as the economy goes through its normal business cycle of ups and downs. And then business lay off and then rehire workers, these people have a place to go. They don’t sit idle in the unemployed pool. They work in a pool of employed people.

“The Job Guaranteeprogramme performs the task of a genuine automatic stabiliser; no government bureaucrat has to decide whether to spend when unemployment increases. No bureaucrat has to decide; it happens automatically. If you become unemployed and you would like to participate in the Job Guarantee programme, you show up and you’re assigned a task and paid a wage. You may receive training while you’re in the programme. When the private sector recovers and begins hiring again, workers will flow out of the Job Guarantee pool and back into other forms of employment. In this way, the Job Guarantee is a buffer stock programme. It buffers the economy against the inevitable economic cycle. So, society gets workers performing useful tasks; the people get to do something useful that makes them feel like they are contributing members of society. They have wages and benefits instead of nothing or a very minimum with probably no benefit.

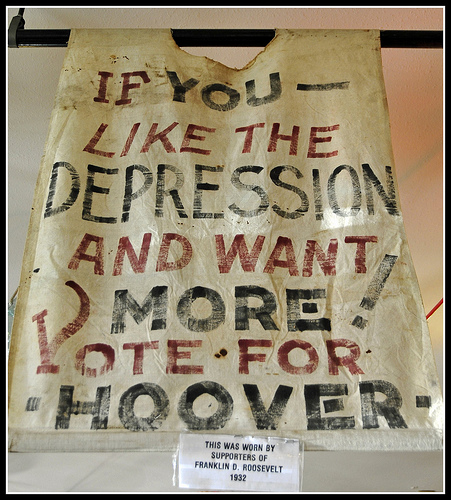

“We’ve never had a Job Guarantee programme in the U.S. But we did have an interesting programme that did many of the same kinds of things. Someone in the audience asked yesterday about Roosevelt’s New Deal. When Franklin Delano Roosevelt was president and the U.S. economy was in the throes of the Great Depression, Roosevelt instituted an alphabet soup of jobs programmes: the WPAwas the Works Progress Administration, my grandfather, one of them, worked in the WPA; the CCCwas the Civilian Conservation Corps. Some of you have asked about environmental problems and whether MMT has anything to say about environmental policy or energy policy. The CCC was very much concerned with the environmental aspects. The NYAwas the National Youth Administration. This was a programme designed, specifically, to deal with the problem of youth unemployment, which we know is a very serious problem in many parts of Europe today.

(c. 22:59) “Roosevelt’s programmes hired the unemployed, gave them a wage, and gave them something useful to do. They built hospitals, schools, parks, bridges, roadways, airports, stadiums, and much, much more. They rebuilt America. The programmes employed millions of Americans in productive and socially useful jobs. Builders, architects, engineers, and even painters, poets, and actors were employed in these programmes. But this is something on a huge scale. It requires the ability to run large government deficits. It requires sovereign money. With sovereign currency and a commitment to functional finance, people can design a democracy that works for them.

“When the people understand this, it eliminates for the policymaker their excuse for not acting. They cannot say, we don’t have the money to do it. Whatever is physically possible is financially feasible. The only constraints that we concern ourselves with, in MMT, are real constraints. We have already overcome in our minds, because of the monetary system and our understanding of it, the financial constraints. They don’t exist. The issuer of the currency can mobilise resources to achieve public purpose. In any democracy, the people should decide what that means. As long as the real resources are available—when I say real resources, I mean the land, the cement, the steel, the real things you need to build roads and bridges and airports and schools, whatever it is that you decide you want and need as a people—as long as those things are available, the government, through its power to tax and spend and power to control its currency, can mobilise those resources for the benefit of all.

“Certain activities are simply too important to be left entirely to markets and their profit motive, as orthodox economics would have it. Care for the environment, energy security, healthcare, income security for the elderly and the dependent, and so on, and so on, are too important to be left to market forces. MMT shows us all that a new and better world is possible.

(c. 26:15) “Okay, so I’m going to turn to a very important concept in MMT—the use of sectoral balances to analyse what’s happening to the financial positions of different sectors in the macroeconomy. We’re gonna begin by recognising that deficits are normal. Capitalist economies, many capitalist economies, run permanent deficits. Surpluses are rare and fleeting in many large, rich countries in the world. For some countries, the deficit emerges the ugly way. The deficit appears because the economy is in trouble. A recession causes rising unemployment and falling income. When incomes fall, tax revenues drop off; deficits explode. You’ve all seen that. There’s an even uglier way to run a deficit and that is to implement fiscal austerity—recession by design. And then there are the good deficits, the kind that MMT understands, doesn’t worry about, and supports. The government can run a deficit by allowing its budget to expand and contract without any arbitrary limit to its size or to the time-frame, under which the deficit is allowed to be sustained.

(c. 28:10) “With the kinds of policies that I’ve outlined, Job Guarantee and beyond, these may require the government to run deficits most, or even all, of the time. So, the question is: Is that good economics?”

Bonnie Faulkner: “You’re listening to professor and research scholar, Stephanie Kelton. Today’s show: ‘Modern Money Theory Explained.’ I’m Bonnie Faulkner. This is Guns and Butter.

Dr. Stephanie Kelton (c. 28:44): “A deficit hawk, we call them in the United States, is someone who is opposed to the deficit on principle. A deficit hawk often favours what they call ‘sound money,’ a gold standard, a monetary union. A deficit hawk would legislate rules that mandate balanced budgets at all times. A deficit hawk believes that there’s no such thing as a good deficit. And a deficit hawk supports immediate austerity to sharply reduce budget deficits.

“A deficit dove is a friendlier bird. A deficit dove supports limited deficit spending in tough economic times. But the doves want the government’s deficit balanced over the business cycle. Deficits in bad times, surpluses in good times, balanced over the cycle.

“A dove supports rules to limit or constrain government spending. Think of the Stability and Growth Pact, which allows small deficits, but also expects surpluses over the cycle. A deficit dove recognises that the deficit is important when the economy turns down and they’re willing to run the deficit in difficult times. But they want austerity after the economy recovers. What are they worried about?

“Both the hawks and the doves are worried about the negative consequences of running a deficit. They are convinced that, at some point, markets will refuse to lend at reasonable rates; interest rates will spike; the debt will become unsustainable; and they think that running large deficits will eventually lead to serious inflation. Paul Krugman is a deficit dove. MMT knows better.

“If the government takes advantage of its status as the issuer of the currency, the government could finance its deficit without borrowing at all. It could be done with no bond sales. This means no discipline from the bond markets. No bond market vigilantes. No solvency problem to deal with. Interest rates would be lower, not higher, as [Paul] Krugman would suggest.

“But what about inflation from running the economy too hot? MMT doesn’t recommend that you run the economy too hot. MMT recommends using deficits to bring the economy up to full employment, not to push it beyond. This is a common criticism that we deal with from our critics who say we want huge deficits and beyond full employment and we never want them to stop and they’ll always be large, and, therefore, we must be insane.

“So, they mischaracterise us, so they can mock us. Functional finance calls upon the government to maintain full employment and price stability. We are as concerned with inflation, as anyone. But we don’t view it as a serious problem when the economy is operating far below full employment with lots of available unused resources. The government has plenty of space to push the economy before inflation should become a relative concern.

(c. 33:18) “Okay, MMT emphasises that you cannot examine, weigh in on, give opinion to, make statements about the size of the government’s deficit or budget overall in isolation. You cannot look at just one sector in the economy when we have a multisector economy. You need to understand how the government’s budget is related to the rest of the economy. To do this, we need a basic understanding of sectoral balances.

(c. 34:03) “So, what did the sectoral balances show? In any given period, they show whether a particular part of the economy is spending more than its income—running a deficit—spending less than its income—running a surplus—or spending just equal to its income—balancing its budget. We have to look at three sectors: two internal sectors—domestic sectors—and one external sector. The internal sectors are your domestic private sector—the combination of all the households and firms in the country put together for analytical purposes—and the domestic public sector—local, state, provincial governments, national government. Outside of the domestic sphere is the external sector. This is the rest of the world. We can call it the foreign sector, foreign governments, foreign households, foreign businesses.

(c. 35:20) “So, we have three sectors and two rules. The two rules are that all three sectors cannot be in surplus at the same time. And all three sectors cannot be in deficit at the same time. These are not my rules. These are the rules of accounting. One person’s surplus is another person’s deficit. The only way for one sector to run a positive balance is for at least one other sector to run a negative balance. You might think of having three coins: heads is positive, tails is negative. Hold three coins in your hand and flip all three, if they all come up heads, throw it out; it won’t work. If they all come up tails, throw it out. You can have two heads and a tail—two surpluses and a deficit—or two tails and a head—two deficits and one surplus.

(c. 36:38) “Balance sheet rules apply. Instinctively, we probably think there’s something inherently better about being in a surplus position. But, remember, we can’t all be in surplus at the same time. It defies the laws of accounting. At least one sector must be in deficit.

(c. 37:09) “Here we see the government sector on the left and the non-government sector on the right. The non-government sector includes domestic households, domestic firms, and the rest of the world, everyone who’s not government. If there’s a surplus in the government sector than, by definition, there is a deficit in the non-government sector. If the government is in deficit, then, by definition, the non-government sector is in surplus.

(c. 37:57) “Two choices: two heads, one tail; two tails, one head. Which one’s better? The private sector needs to be in surplus almost all the time. As a general rule, the private sector cannot survive in a deficit position. Households and firms, as users of the currency, cannot continually spend more than their income. At some point, even the financial wizards of Wall Street will run out of credit-worthy borrowers who are looking to borrow more. When that happens, asset prices go sideways; sales soften; jobless claims go higher; and the economy turns down. Government budget moves into deficit automatically, the ugly way.

“The private sector cannot create net wealth for itself. Businesses, banks, and households together can borrow and lend, but every asset is offset by a liability from someone else in the private sector. The assets and liabilities cancel each other out. We can’t create net financial assets internally by ourselves, as a private sector. Net financial wealth must come from outside the private sector.

“So, where do surpluses come from? Remember that a surplus means that your income exceeds your expenditure. A deficit means you’re spending more than your income. Any one of these sectors—the private sector on the left, the public sector and the foreign sector on the right—any one of them can be in deficit or surplus, but they can’t all be in deficit or surplus together.

“If the government sector is running a deficit, it tends to add to the private sector’s surplus.

“If the rest of the world is running a deficit against Italy, that means Italy has the surplus. Either, a government deficit or a trade surplus will increase the private sector’s net wealth. This is—for those of you who might’ve wondered where the equation came from—it comes from the national income accounting. I’m just showing you, so that you know I’m legitimate. You just move identities around. Trust me, okay?

(c. 41:42) “On one side of the equation, you see where our nation’s income comes from. I call that sources of income. On the other side of the equation, you see how we use our income. Sources and uses have to be equal. We can set these equations equal, move terms to other sides, and write this equation here. Which is the important equation for us?

(c. 42:10) “This is the difference between what the private sector is saving and spending. This is the difference between what the public sector—the government—is spending and collecting. This is the difference between what the rest of the world is buying from you—your exports—and what you are buying from them—imports.”

Bonnie Faulkner: “You’re listening to professor and research scholar, Stephanie Kelton. Today’s show: ‘Modern Money Theory Explained.’ I’m Bonnie Faulkner. This is Guns and Butter.”

Dr. Stephanie Kelton: “I mentioned that if the private sector is going to be in surplus, it requires at least one other sector to be in deficit. This is the actual data for Italy. The red line on the bottom shows the government’s budget balance. You can see that in every year, since 1996, the Italian government has run a deficit. You can also see that the bigger the deficit in the government sector, the bigger the surplus in the private sector. Indeed, they almost look like they move exactly opposite to one another. You could even say that as the government goes down, you go up. That’s a different way to think about the government’s deficit. I’m not making it up.

(c. 44:08) “Here’s Ireland. It looks similar. As Ireland’s government deficit exploded, so did the accumulation of financial assets—savings—in the private sector.

“Greece: similar.

“Spain: as deficits increase—here’s Spain at more than 10% deficit to GDP and here’s the Spanish private sector in surplus.

“Germany: Germany runs surpluses on occasion. But what happened to the private sector? As Germany’s budget moved in to surplus, you can see here in this period where the German budget was in surplus and the private sector was driven into deficit, not some place the private sector usually spends much time because the private sector can’t survive in deficit.

(c. 45:20) “Here’s the United Kingdom, Japan, and the United States. The large deficits that have been run since the downturn in the economy following the financial crisis, huge deficits that have terrified the hawks, have helped the private sector rebuild and repair their balance sheets by adding to their financial savings. This makes for a good deficit. The reason that the two lines were not perfect mirror images in the last set of graphs was because I didn’t include the foreign sector. I just wanted to focus you in on the relationship between the public sector’s deficit and the private sector’s surplus.

“Here is a complete picture for the United States. Every area in red shows you the US government’s budget position. Anything that falls below zero indicates a public sector deficit. You’ll notice that the U.S. government is almost always in deficit. The blue represents the private sector’s balance. You’ll notice that the private sector is almost always in surplus. The green represents the foreign balance. It’s been quite some time since the US ran a positive trade surplus. You can see a few back in the early years. We are now running trade deficits, sometimes, fairly substantial ones. And that reduces the private sector’s surplus.

“So, let’s focus in on a specific period of time. The period in the late 1990s and early 2000s when for the first time in decades the US government ran budget surpluses. You can see those surpluses where the red goes into positive territory. These years here represent government budget surpluses. Many people would inherently think that would be a good thing. It shows fiscal responsibility. Not only did they balance the budget, but they put it in surplus. Meanwhile, our current account deficits were huge. The rest of the world was running large positive balances against the US. That reduced US private- sector savings. Surpluses fell. It pushed the private sector into deficit on an unprecedented scale. The private sector went from surviving above the zero line to being pushed below zero. And the private sector remained there for a period of years, spending more than its income, borrowing to do it. And it was all fueled by a massive bubble economy that ended in recession, which drove the public sector’s balance back into deficit where it belongs.

(c. 49:16) “Okay, the last part that I want to introduce this morning is the Financial Balance Model. We are very excited in the MMT world about this model. It was developed by a friend of ours, who is an outstanding economist. His name is Rob Parenteau. He writes on the New Economics Perspectives blog. And he came up with this model. And it is the framework that allows us to compare all three sectors’ budget positions in a graph. Economists like graphs. So, in fact, it’s how you gain credibility in our world. So, one must use models and graphs.

(c. 50:15) “The vertical axis measures the public sector’s budget position. If the government is in surplus, we’ll be in the top half of the graph. If the government is in deficit, we’ll be in the bottom half of the graph. The horizontal axis measure’s the current account, the foreign balance.

“If you’re on the right half of the graph, the current account is in surplus.

“If you’re on the left half of the graph, the current account is in deficit.

“The dashed line shows the private sector’s financial balance set at zero.

“So, every point along the dashed line is a point where the private sector has no surplus and no deficit—spending equals income. Above the dashed line, the private sector is in deficit. Remember what I said: The private sector cannot survive in that territory. Below the dashed line, the private sector is in surplus. Okay?

(c. 51:39) “For a country that issues a sovereign currency, fiat money, no fixed exchange rate, the world is your oyster. You can be anywhere in the graph. There are no rules or reasons that you can’t be located anywhere. But remember the diagonal line, anywhere above that is unsustainable for the private sector. So, the only sustainable space is below that line, the green line.

“What about here for countries that use the euro? Where are you supposed to operate? Well, if you’re playing by the rules, your deficit is not supposed to exceed 3% of your GDP. So, we put in a lower bound at 3%, negative. This is the space that’s available—in theory. What about countries in the Eurozone that run current account deficits? Remember that current account deficit is every where to the left of the vertical line, but you can’t go below 3%. So, countries with a current account deficit, they get that rectangle. Countries that run current account surpluses have a different space. A country with a current account surplus can put its private sector in surplus with a smaller public sector deficit.

“Here’s the situation for a country that uses the euro and also runs a current account deficit. Can you see it? It’s a small space. This is the space that you are given to work with. Anything above the dashed line means a private sector deficit. It’s not a sustainable space for you, for any of us. You must be below the dashed line. But you must also be above the red line. But because you’re running a trade deficit, you’re also to the left of the vertical line. You get only to play in that little triangle.

(c. 54:30) “So, lets talk about what’s happened to Italy. Germany has crushed many members of the Eurozone through its labour policies that began in the early 2000s. Marshall [Auerback]talked last night about the Hirsch Commission and in Agenda 2012, which was Chancellor Schröder’seconomic miracle, whereby Germany ‘reformed’ its labour markets by reducing the power of their labour unions and their craft guilds making it easier for their employers to fire people at will, cut unemployment benefits, so that German benefits last about half as long as benefits in the US. They were harsh ‘reforms.’ And as they were being implemented, unemployment, initially, increased. It hurt the German economy, but not for long because that pain was soon transferred to others.

(c. 55:45) “So, I want you to look at this picture: Italy, in 1996, was running a trade surplus of more than 3% of your GDP. You had more fiscal space before the German policies. And now you have that little triangle. It doesn’t give you enough policy space without breaking the Stability and Growth Pact rules it is extremely difficult for you to keep the private sector in surplus and the economy healthy. I would say it’s impossible.

(c. 56:22) “Italy makes it into the small triangle, but not often. Most of the time, though, your deficits have been large enough to compensate for the trade deficits that you run and you’ve been able to keep your private sector in surplus. But that’s because the rules were broken. If you had played by the rules, for the last 14 years, you would have been successful three times.

“Ireland would never be successful. The space is just too small.

“You see Greece. The triangle for Greece is way up in the corner. They can’t play by these restrictive rules, either.

(c. 57:05) “Same problem for Spain.

“Germany, on the other hand does brilliantly, almost every point is to the right of the green line where the private sector is in surplus. Although, Germany breaks the Stability and Growth rules, like everyone else. It’s the large current account surpluses that Germany runs, thanks to all of you. It’s the secret to their success. It’s why they can run smaller deficits, stay out of trouble. You are financing it.”

Bonnie Faulkner (c. 57:57): “You’ve been listening to professor and research scholar, Stephanie Kelton at the Summit on Modern Money Theory in Rimini, Italy. Today’s show: Modern Money Theory Explained.

“Stephanie Kelton is Associate Professor of Economics at the University of Missouri, Kansas City, Research Scholar at the Levy Economics Institute, and Director of Graduate Student Research at the Center for Full Employment and Price Stability.

“She is Creator and Editor of New Economic Perspectives. Her research expertise is in Federal Reserve operations, fiscal policy, social security, healthcare, international finance, and employment policy.

“Please visit the University of Missouri, Kansas City New Economic Perspectives blog at www.NewEconomicPerspectives.org. Visit the website for the first Italian Summit on Modern Money Theory at www.DemocraziaMMT.info.

“Guns and Butter is produced by Bonnie Faulkner and Yara Mako. To leave comments or order copies of shows, email us at [email protected]. Visit our website at www.gunsandbutter.org.”

Transcript by Felipe Messina for Media Roots and Guns and Butter

MEDIA ROOTS — In order to move from a liberal capitalist society, organised around elite interests, to a socialist political and economic system run by and for working people, the problem of false consciousness among the USA’s working-class must be confronted, argues Dr. Jeremy Cloward of Diablo Valley College in his paper entitled “The State, Class And False Consciousness Within the American Working Class.”

Messina

***

PROJECT CENSORED — In the United States the American working class has seen itself become increasingly involved in fighting imperialistic wars abroad, financing a growing military budget, and losing its social safety net at home yet at the same time regularly acting politically inconsistent with their own class interests. This has been to the gain of US-based multinational corporations and to the detriment of working people. Until the working class in the United States realizes that the predominantly corporate-controlled state does not serve their personal and class interests they will not see any significant improvement in their lives. On the contrary, as long as working people continue to support the two major parties they can expect to see many more years of corporate dominance of the United States political, economic and social system. The primary issue that working people must address to resolve this problem is the question of false consciousness.

False Consciousness

False consciousness is a term derived from the Marxist tradition which identifies a state of mind of an individual or a group of people who neither understand their class interests nor act politically consistent with those concerns. Karl Marx, himself, did not use the term false consciousness. However, many who are intellectually aligned with the Marxist tradition trace the concepts’ origin back to a theory first developed by Marx known as commodity fetishism. Commodity fetishism is the idea that people place a value on commodities apart from the ones which they intrinsically possess. For example, a diamond, once it becomes a commodity, is not simply a rock with the properties of a rock but instead an object that people value and admire as if the rock possessed some built-in power which makes it different and more valuable than any other rock.

False consciousness as a concept was first used by Marx’s friend and collaborator Friedrich Engels in July of 1893 in a letter to Franz Mehring. While writing about the concept of historical materialism he claimed that “ideology is a process accomplished by the so-called thinker consciously, indeed, but with a false consciousness. The real motives impelling him remain unknown to him; otherwise it would not be an ideological process at all.”[2] Thus Engels, in two brief sentences coins the term and argues that false consciousness and ideology (i.e., worldview) are intellectual constructs.

MEDIA ROOTS — Pacifica Radio’s Guns and Butter have faithfully broadcast another potent weekly instalment of compelling discussions from the radical economics summit in Rimini, Italy produced by journalist Paolo Barnard: Summit Modern Money Theory 2012. Media Roots previously transcribed and featured the first, second, third, and fourth consecutive Guns and Butter broadcasts on the MMT Summit. Here we present the most recent coverage of this important and inspiring international economic summit featuring academic Dr. William K. Black, author of The Best Way to Rob a Bank Is to Own One.

It’s essential to understand, at least, the basics of how the ruling-class widens inequality. It’s equally important to understand our role in perpetuating that widening inequality by supporting their corrupt political parties, the Democrat and Republican parties, and their counterparts abroad, for which no amount of token reformers, such as Dennis Kucinich or Paul Wellstone or Barbara Lee or you name it, could compensate because corporate funding isn’t intended to benefit the working-class. Dr. Black discusses many economics taboos never mentioned. Similarly, we must acknowledge political taboos never mentioned, such as our rigged two-party system. The days of New Deal Democrats are long gone. It’s high time for expanding beyond U.S.A.’s monopolised two-party dictatorship, which undergirds the vast fraud Dr. Black discusses, as well as virtually every other single-issue, which atomised activists toil against. As U.S.A. faces the masochistic prospect of electing another pro-1% Republican or re-electing the pro-1% Democrat Obama, we bear in mind the role of political parties and their principles, or lack thereof, and our atrophied votes for the least worst, rather than the best possible. (Transcript below.)

Messina

***

GUNS AND BUTTER — “And here’s the key question: How many of you are bankers? Not many, right? How much brains does it take to make a bad loan? I think we could all do that. So, all the mediocre bankers have no way to make money with honest competition. But they have a sure thing, if they’re willing to follow the fraud recipe.” —William K. Black

“I’m Bonnie Faulkner. Today on Guns and Butter: William K. Black. Today’s show: ‘Formula For Fraud.’ William Black is Associate Professor of Law and Economics at the University of Missouri, Kansas City. He is a lawyer, academic, and former bank regulator and author of The Best Way to Rob a Bank is to Own One: How Corporate Executives and Politicians Looted the S&L Industry.

“In today’s show, Black deconstructs the elements, that constitute the recipe for fraud.”

Dr. William K. Black (c. 2:05): “It’s difficult to follow such a raging optimist. [Applause] But I can assure you, it’s actually far worse than they say. First, there are no ‘technocrats,’ especially the ‘genius’ technocrats. I suggest a new rule of thumb for judging a ‘genius technocrat.’ They have to be right at least two out of ten times. And there’s not a single economist in Europe, who calls himself a technocrat, that could do the equivalent of making two penalty kicks out of ten. So, I’m going to pick up on some of the things, that Michael [Hudson] has talked about. He quoted Balzac’s famous phrase that behind every fortune lies a great scandal. And I’m going to explain how that works. So, you will now learn how to steal €10 billion euros. [Applause] The purpose of this is not so that you will steal €10 billion euros. The purpose is so that you can be an intelligent lion because they feed on sheep.

(c. 3:40) “We’ve been asked to do our talks in four parts. So, unlike Gaul, my speech is divided in four parts. This talk will be about why we suffer recurrent, intensifying, financial crises. Then, I’ll explain how theoclassical economic dogma produces these disasters. The third part will be to explain why our response to the crisis has made it worse. And I, actually, will end on an optimistic note. The fourth part is how we have succeeded in some places at some times and why you can do the same.

(c. 4:29) “Part one sounds like one question: Why do we have recurrent, intensifying, financial crises? But it’s really two questions. The first one asks: What is the cause of these crises? The second one says: Well, wait a minute. We keep on suffering crises. Why don’t we learn the right lessons from these crises? So, part one will focus on what caused the crises.

(c. 5:05) “Part two will focus on why ideology prevents us from learning the right lessons.

“Santayana’s famous phrase, of course, is that those that forget the mistakes of the past are condemned to repeat them. But, even if we remember the mistakes we’ve made, the new policy we pick could be another mistake. So, part three discusses that, in part.

“But part four says the real tragedy is when you forget the successes of the past, when you have something that you know works and that you refuse to use. Because, as Michael [Hudson] said, there’s not an economics textbook in the world, that warns you that elite CEOs often become wealthy through fraud. And there is a primitive, tribal, taboo in economics in English against using the five-letter eff-word—fraud. When I go and talk to groups of economists, who are traditional, I start out the meeting by asking them each to say out loud the word fraud. You can’t believe how difficult it is for them, even, to utter the word.

(c. 6:42) “So, as I said, the lessons of success, it’s a real tragedy to forget them. And I’m going to quote from George Akerlof and Paul Romer’s famous article, or, at least, an article, that should be famous where the title says it all: ‘Looting: The Economic Underworld of Bankruptcy for Profit.’ So, the bank fails or, in the modern era, is ‘bailed‘ out, but the CEO walks away wealthy. And this is what Akerlof and Romer wrote about 20 years ago:

“‘Neither the public, nor economists foresaw that savings and loan deregulation was bound to produce looting, nor, unaware of the concept, could they have known how serious it would be. Thus, the regulators in the field who understood what was happening from the beginning found lukewarm support, at best, for their cause. Now, we know better. If we learn from experience, history need not repeat itself.’

(c. 8:22) “George Akerlof was awarded the Nobel Prize in Economics in 2001. So, you might think economists would pay attention. You might think, since this article was written nearly 20 years ago, that the textbooks would mention fraud and looting. They don’t just ignore everyone here. They ignore Nobel Prize winners in Economics.

“So, what, again, was this lesson? It was the regulators in the field, the little people, not the fancy people, who understood from the beginning that deregulation would lead to massive looting. And it was the economists, that ignored them. And after we had proven that it was fraud, after we had sent over a thousand elite bankers and their cronies to prison, after a Nobel Prize winner warned about it, after all those things, they ignored it and produced crisis after crisis, including the one we experience now.

(c. 9:59) “So, what did we know out of that savings and loan crisis, that was widely described at the time as the worst financial scandal in U.S. history? And we have a history rich in scandal. Here is what the national commission, that investigated the causes of the crisis reported:

“‘The typical large failure [grew] at an extremely rapid rate, achieving high concentrations of assets in risky ventures… [E]very accounting trick available was used… Evidence of fraud was invariably present, as was the ability of the operators to ‘milk’ the organisation.’

(c. 11:04) “That means to loot the organisation. But, speaking of milk, [Applause] the frauds I’m describing are in no way limited to the Unites States; they exist in every country. And they are common enough to explain, and they are old enough to explain, what Balzac was saying because many of the wealthy become rich through precisely the scandals, the fraud, I will describe.

“In criminology, we call them financial super predators when we’re being lyrical. When we’re writing journals, we call them ‘control frauds,’ which is boring. Control fraud occurs when the person who controls a seemingly legitimate entity, like Parmalat, uses it as a weapon to defraud. And they can often use this weapon with impunity. In finance, accounting is the weapon of choice.And these accounting frauds cause greater losses than all other property crimes combined; yet, economics, again, never talks about it. Worse, when many of these frauds occur in the same area, they hyperinflate financial bubbles, which is what causes financial crises and mass unemployment. It makes the CEOs wealthy, produces Balzac scandals, and destroys democracy.

(c. 13:10) “In criminology, we talk about criminogenic environments, long words, simple concept. When the incentives are extremely perverse, you will get widespread fraud. So, what makes for perverse incentives? The ability to steal a lot of money and not go to prison and not having to live in disgrace. In practice, that means, in English, the three Ds: deregulation, desupervision, and de facto decriminalisation. Deregulation: You get rid of the rules. Desupervision: Any rules, that remain, you don’t enforce. Decriminalisation: Even if you sometimes sue them and get a fine, you don’t put them in prison. So, that’s the first area—deregulation.

(c. 14:20) “The second area is executive compensation.And what is ideal for accounting fraud? Really high pay based on short-term-reported income with no way to claw it back, even when it proves to be a lie. Those are the most important, but it’s also good, if your assets don’t have a readily verifiable market-value ‘cos then it’s easy to inflate the asset prices and it’s easy to hide the real losses. And, if you want a true epidemic of fraud, if entry into the industry is very easy, then you’ll get much more fraud.”

Bonnie Faulkner (c. 15:15): “You’re listening to lawyer, academic, author, and former bank regulator William K. Black. Today’s show: ‘Formula for Fraud.’ I’m Bonnie Faulkner. This is Guns and Butter.”

Dr. William K. Black: “So, this is what you were waiting for, at least from me. This is the recipe, only four ingredients, that bankers in many parts of the world use to become billionaires. And, again, it’s one that Akerlof and Romer agreed with. So, first ingredient: grow massively. Two: by making really, really crappy loans, but at a higher interest rate. Third ingredient: extreme leverage—that just means a lot of corporate debt. Fourth ingredient: set aside virtually no loss reserves for the massive losses that will be coming. By the way, in Europe, this last ingredient is mandated by international accounting rules, which are incredibly fraud-friendly. And everybody knows that—in accounting—and nobody has changed it. If you do these four things, you are mathematically guaranteed to report record short-term income. This is why Akerlof and Romer referred to it as a sure thing—it’s guaranteed.

(c. 17:10) “There are actually three sure things. The bank will report record profits. The profits, of course, are fictional. The CEO will promptly become wealthy and, down the road, the bank will suffer catastrophic losses. Again, if many banks do this, you will hyperinflate a bubble. This recipe helps explain why bankers hate markets, why bankers hate capitalism, why they hate anything like an effective market.

“So here’s a thought exercise: What if you were a CEO of a bank and you wanted to grow exceptionally rapidly? The first ingredient to the fraud recipe, that means 50% a year. And that’s realistic; that’s what the banks in Iceland, that’s what many of the banks in Europe—continental Europe—and the US also did. How would you do that if you were honest? You’re in a market that’s competitive. The only way to grow that rapidly is to charge far less money—a lower interest rate—for your loans. But if they’re a real market what would your competitors do? They would match your price reduction. You wouldn’t end up making any more loans; and all the banks would be loaning at a lower interest rate. So, here’s the question? Is that a good way to make money as a bank? It’s a terrible thing for a bank, right? So, all the bankers would lose. And that’s why they hate markets. And that’s why banks are the biggest proponents of crony capitalism and the leaders worldwide in crony capitalism.

(c. 19:26) “And that leads us to a discussion of why bad loans are so perfect for bank fraud; you can charge a much higher rate to people who can’t get loans because they can’t repay the loans. And there are millions, tens of millions, of such people. So, you can grow very rapidly. You can charge a higher interest rate. If your competitors do the same thing, it’s actually ‘good’ for you because it hyperinflates the bubble. And the bad loans, you just refinance them and you hide the losses for many more years.

(c. 20:22) “So, the CEO takes no risk; all of this is a sure thing. And here’s the key question: How many of you are bankers? Not many, right? How much brains does it take to make a bad loan? I think we could all do that. So, all the mediocre bankers have no way to make money with honest competition. But they have a sure thing, if they’re willing to follow the fraud recipe. I’m now gonna quote from the person, the economist [James Pierce, NCFIRRE’s Executive Director], who led the national investigation of the savings and loan crisis. And he called this dynamic I’ve just explained, ‘the ultimate perverse incentive.’ So, this is what he said:

(c. 21:28) “‘Accounting abuses also provided the ultimate perverse incentive: it paid to seek out bad loans because only those who had no intention of repaying would be willing to offer the high loan fees and interest required for the best looting. It was rational for operators’—that’s CEOs—‘to drive their banks ever deeper into insolvency, as they looted them.’

(c. 22:12) “That is how crazy a world that theoclassical economics has built, where the best way, the surest way, to become wealthy, as a bank CEO, is to make the worst possible loans. And to make so many bad loans, they have to gut the underwriting process. Underwriting is what an honest bank does to make sure that it’s going to get repaid. But, if you want to make bad loans, you have to get rid of your effective underwriting. So, this is the key, if you get rid of underwriting. We already established you’re not bankers.

“So, imagine all of you run Competent Honest Bank and you do underwriting. And you can tell can tell high-risk and low-risk borrowers. Low risk borrowers you charge 10%. High-risk borrowers you charge 20%. I run Bill’s Incompetent Bank, I can’t tell risk. So, I charge everybody 15%. Which borrowers come to me? Only the absolute worst borrowers. No good borrower would come because they could borrow at your bank at 10%. So, this is not like a usual risk. In economics, we call this adverse selection. And it means that a bank, that makes loans this way must lose vast amounts of money. No honest banker would operate this way. And the banks, that engage in these frauds, also create criminogenic environments, themselves, to recruit fraud allies. For example, the people, that value homes. If they won’t inflate the value, the dishonest banks won’t use them. Do they need to corrupt every person that values homes? No. 5% of the profession would be fine. They just send all their business to the corrupt—we call them—appraisers in America. And this is called a Gresham’s Dynamic; and it means that cheaters prosper and bad ethics drives good ethics out of the marketplace.

(c. 25:18) “Well, what about compensation? In [the United States of] America, the largest corporations, the largest 100, created a group to lobby, called the Business Roundtable. And you remember our Enron-era frauds, early 2000s? Well, they got embarrassed. And, so, they appointed a task force to look at the frauds. And they named a particular CEO as head of their task force; and he was asked by Business Week, why do we have all these frauds? This is the answer he gave:

“‘Don’t just say: ‘If you hit this revenue number, your bonus is going to be this.’ It sets up an incentive that’s overwhelming. You wave enough money in front of people; and good people will do bad things.’

(c. 26:28) “And that was Franklin Raines, the head of Fannie Mae, which is now insolvent by about $500 billion dollars. How did Frank Raines know about this perverse incentive? Because he used it at Fannie Mae to produce the frauds, that made him wealthy.

“How about Ireland? This is a report by a Scandinavian banker hired to do an investigation, not a real investigation, of course. He reported:

“‘Bonus targets, that were intended to be demanding through the pursuit of sound policies and prudent spread of risk were easily achieved through volume lending to the property sector.’

(c. 27:25) “Now, that requires a translation, not because it’s written in English, but because it’s written to be not understood. So, what is he really saying? The bank CEO sets a target for income, that is huge—three times the current income. How can you triple income safely? Wow, if somebody could really do that safely, we’d be happy to pay them a very big bonus, right? But what does he say?

“You don’t have to do it safely. And it isn’t hard. You just follow the fraud formula, the recipe, and it’s a sure thing. It’s easily achieved.

“What’s wrong with his sentence, though?

“He says the targets were intended to be difficult, demanding. And they were intended to be met through prudent lending.

(c. 28:34) “Seriously, you think that? The CEO is deciding how much money he is going to make. Do you think he intended a demanding target or a target that was easily achieved and would make him wealthy?

“So, I will end on this. We need a coast guard for our banks. We can no longer allow CEOs to desert their posts after running their banks aground and causing such great destruction. The cruise ship’s captain’s career is over. But the elite bank CEOs, that destroyed the global economy remain wealthy, powerful, and famous because they looted. They were ‘bailed’ out. They did not leave in a lifeboat in the dark of night. They left in their yachts, yachts that the governments paid for. And no official anywhere in the world has demanded of those bank CEOs who deserted their vessels […] [Applause] Grazie.”

Bonnie Faulkner (c.30:30): “You’re listening to lawyer, academic, author, and former bank regulator William K. Black. Today’s show: ‘Formula for Fraud.’ I’m Bonnie Faulkner. This is Guns and Butter.”

Dr. William K. Black: “Someone called on the Black Plague? I’m here. [Laughter, Applause]

“In this part two, I’m going to talk about why we have recurrent, intensifying crises, why we don’t learn the right lessons from our past crises. And then we’re going to discover something that, of course, you’ve been hearing. The dominant economists are truly terrible at one thing. They are terrible at economics. But occasionally they go beyond economics and they are abysmal on ethics. And they are the leading opponents and dangers to democracy throughout the EU, in particular, but in America as well.

(c. 31:40) “Economists tell us they want to be judged on their predictive ability. We welcome their admission because their record in prediction is pitiful. But, of course, it is precisely the fact that they’ve been wrong about everything important for three decades, that makes them unwilling to admit their error and evermore insistent on continuing their worst policy advice.

(c. 32:12) “As I said economics is particularly awful when it gets into the concept of morality. In my first talk, I read you a quotation from the economist who conducted the study of the savings and loan crisis. And he pointed out that it was ‘rational’ for looters to make bad loans. Well, here is the reaction of one economist, Greg Mankiw, to hearing the work of that national commission and of that Nobel Prize winner-to-be, George Akerlof. He listened to their story and he said—and this is not an off-hand comment; he was the official discussant; he had the paper a week in advance; he thought about these remarks—he said:

“‘[…] it would be irrational for savings and loans [CEOs] not to loot.’

“So, note that he goes from simply a statement about how you maximise fraud by making bad loans to the ethical proposition that if it would be rational action, it must be the appropriate action, even though the rational action is to defraud.

(c. 33:40) “Now, there’s a very interesting book called Moral Markets, that had the unfortunate timing to come out in 2008 because it is a triumphal book about capitalism and about how capitalism makes markets more moral. But even it contains this statement:

“‘Homo economicus is a sociopath. Homo economicus is what happens if people behave the way economists predict that they will behave.’

“And these scholars, who love capitalism, said: if you do that, you will create a nation of sociopaths.

“Greg Mankiw was not a random economist. [Then-]President Bush made him Chairman of the President’s Council of Economic Advisers, the most prominent economic position in America, after he had said these things.

(c. 34:48) “The next two gentlemen are the leading law and economics scholars on corporate law. And I’m quoting from their treatise in 1991; so, an entire generation of US lawyers have been taught this next phrase:

“‘A rule against fraud is not an essential or […] an important ingredient of securities markets.’

“The key economist there—who is not really an economist, he’s a lawyer—isDaniel Fischel. He worked for three of the worst control frauds, including the absolute worst savings and loan ‘control fraud,’ praised them as the best firms in America, and then wrote this two years later without ever admitting in his book that he had tried his theories in the real world and they had led him to praise the worst frauds. So, this is rank academic dishonesty on top of getting everything wrong. And what happened to Fischel after he got everything wrong? He was made Dean of theUniversity of Chicago Law School, one of the most prominent academic positions in America.

(c. 36:15) “Alan Greenspan also worked for the worst fraud in the savings and loan crisis. Charles Keating’sLincoln Savings. And he personally recruited, as a lobbyist for this worst fraud, the five [bipartisan] US Senators who would intervene with us to try and prevent us from taking enforcement action against the largest violation in the history of our agency because that violation was by Charles Keating and Lincoln Savings. And those five senators became known and ridiculed as the Keating Five. By the way, [Republican Senator] John McCain was one of those senators who met with us. [The other four were Democrats.]

“Alan Greenspan then wrote a letter saying we should allow Lincoln Savings to do these terrible investments because ‘they posed no foreseeable risk of loss to the federal insurance fund.’ Lincoln Savings proved to be the largest cost to the insurance fund. After he had gotten it as wrong, as it is possible to get something wrong, we made him Chairman of the Federal Reserve. So, here you have a record of we promote and honour, in economics, the people who get it spectacularly wrong, as long as they get it wrong for powerful banks, that are frauds.

(c. 37:59) “So, what did they predict? This is the short list. Neoclassical economists predicted, that because markets were efficient they were self-correcting, fraud was automatically excluded, and financial bubbles could not occur.

“They assured us that because of bankers’ interest in their reputations and auditors and appraisers, that they would never commit a fraud and never assist a fraud.

“They predicted that massive financial derivatives would stabilise the economic system.

“They told us, even when the bubble had reached proportions larger than any in the history of the world, that there was no housing bubble in the United States, that there was no housing bubble in Ireland, that there was no housing bubble in Japan, that there was no housing bubble in Spain.

“They told us that if we paid CEOs massive amounts of money based on short-term performance, that was fictional, it would align the interests of the CEO with the shareholders and the public and be the best possible thing.

(c. 39:30) “Every one of these predictions proved utterly false. Actually, every single one of these predictions had been falsified before the economists ever said them; and they did not change.

“What did they do back in the day? They looked at Europe. This is Cato, named, of course, after a famous Roman—a very conservative anti-think tank in the United States. Cato, in 2007, as Iceland was collapsing in massive fraud, said these words:

“‘Iceland’s economic renaissance is an impressive story. Supply-side reforms’—that means tax cuts—‘along with policies, such as privatisation and deregulation, have yielded predictable results.’

“Remember, we’re making predictions.

“‘Incomes are rising, unemployment is almost non-existent, and the government is collecting more revenue from a larger tax base.’

“So, they cut taxes, but overall tax revenue grows because the country is growing at a massive rate. Why? Because the big three banks in Iceland are all accounting control frauds. They are growing at an average rate of 50% every year. And by the time they collapse in 2008, they are ten times the GDP of Iceland. And they suffer 60% losses on their assets. That was their prediction of proof-positive that deregulation, low taxes, privatisation produce economic booms.

(c. 41:36) “They said something very similar about Ireland in an article entitled ‘It’s Not Luck‘:

“Ireland […] boasts the fourth highest gross domestic product per capita in the world. In the mid-1980s, Ireland was a backwater with an average income level 30% below that of the European Union. Today, Irish incomes are 40% above the EU average.

“‘Was this dramatic change the luck of the Irish? Not at all. It resulted from a series of hard-headed decisions that shifted Ireland from big government stagnation to free market growth.’

“And they wrote this in 2007, a year after the Irish bubble had popped and Ireland was going into freefall. And what are we being told now is the answer? Hard-headed decisions, that shift the governments from big government stagnation to free market growth. They have learned absolutely nothing from their past failed ‘predictions.’ In fact, Trichet came to Ireland in 2004 and said Ireland should be the model for nations joining the European Union.”

Bonnie Faulkner (c. 43:20): “You’re listening to lawyer, academic, author, and former bank regulator William K. Black. Today’s show: ‘Formula for Fraud.’ I’m Bonnie Faulkner. This is Guns and Butter.”

Dr. William K. Black: “But we have seen this movie many times before in many countries. We had seen it in the Savings and Loan Crisis. But then came the Enron-era Crisis and WorldCom. And I’ll focus on just one aspect. Again, we had accounting control fraud, that drove an immense crisis. But what people forget is that most of the world’s largest banks eagerly aided and abetted Enron’s frauds. They knew Enron was engaged in fraud; and they thought that was a good thing because they would get more deal flow, as we say, more volume. These frauds were documented extensively by investigations, hundreds of pages about it. Not a single one of the large conventional bankers were prosecuted. There was a prosecution about Merrill Lynch, which the courts obstructed. Indeed, the U.S. Supreme Court ruled that only the government could bring civil suits—against an enforcement action, of course—against banks, that aided and abetted fraud. Think of that! You could have indisputable proof that the bank had aided Enron, knowingly done so, caused you billions in losses, and you could not sue the bank. That’s how bad the law has become in the United States.

(c. 45:27) “So, that left us with, Will the government sue? Well, the Federal Reserve, we now know from recent testimony in front of the national commission, that investigated this current crisis, the leadership actively resisted bringing any action against the banks, even what we call a slap on the wrist. And it was only when the Securities and Exchange Commission took a slap on the wrist that the Federal Reserve was embarrassed into taking any action.

“We also know, from this extraordinary testimony by the long-time head of supervision at the Federal Reserve, that he was deeply disturbed by the fact that most of the largest banks in the world had aided Enron’s fraud. So, he put together a comprehensive briefing for the leadership of the Federal Reserve. At that meeting, the senior officials of the Federal Reserve and the senior economists of the Federal Reserve did not criticise Enron and they did not criticise the banks that aided Enron’s frauds. They were enraged at the supervisor. How dare he criticise banks? And this was the era—and continues, in the United States, to be the era—of reinventing government, which is a neoclassical, neoliberal, be soft on bankers.

“And I witnessed, personally, when our Washington staff came at a training conference and instructed us that we were to refer to banks as our clients. We were the regulators. And we were, not only, supposed to refer to them as clients, we were supposed to treat them as clients. Being a quiet type, I stood up and began protesting; and they simply shouted us down. [Applause]”

(c. 47:59) “So, this is occurring in 2001, 2002, 2003, 2004. At that point, Italy enters the picture. And Italy enters the picture because of Parmalat. And it enters the picture because, again, you have a massive accounting control fraud where the CEO is looting Parmalat and taking the money out of Italy to tax havens where he can hide it in a wave of special complex corporate forms designed to hide the fraud.

“And what does the Federal Reserve say about all of this? Well, first they brag about their ‘enforcement’ action. Note that they won’t name the large institutions: